My colleague and Fed Chair is in a hard place:

Normally, raising interest rates tightens the monetary supply, making money at T1 worth less than money at T2 and so on, which is the reverse of an inflationary trend. It is deflationary. Since money will be worth more tomorrow than today, up to the margin I will invest less money today relative to tomorrow. Normally this will place downward pressures on employment since I am not going to invest today what I can invest more profitably tomorrow. (Again, under inflationary conditions the reverse holds; since my capital will be worth less — will purchase less — tomorrow than today, I will purchase things today.) Normally.

One of the corollaries to this principle is that, generally, I only tighten the monetary supply when the economy is approaching full employment, which our economy is, thanks almost entirely to quantitative easing (QE) and historically low interest rates.

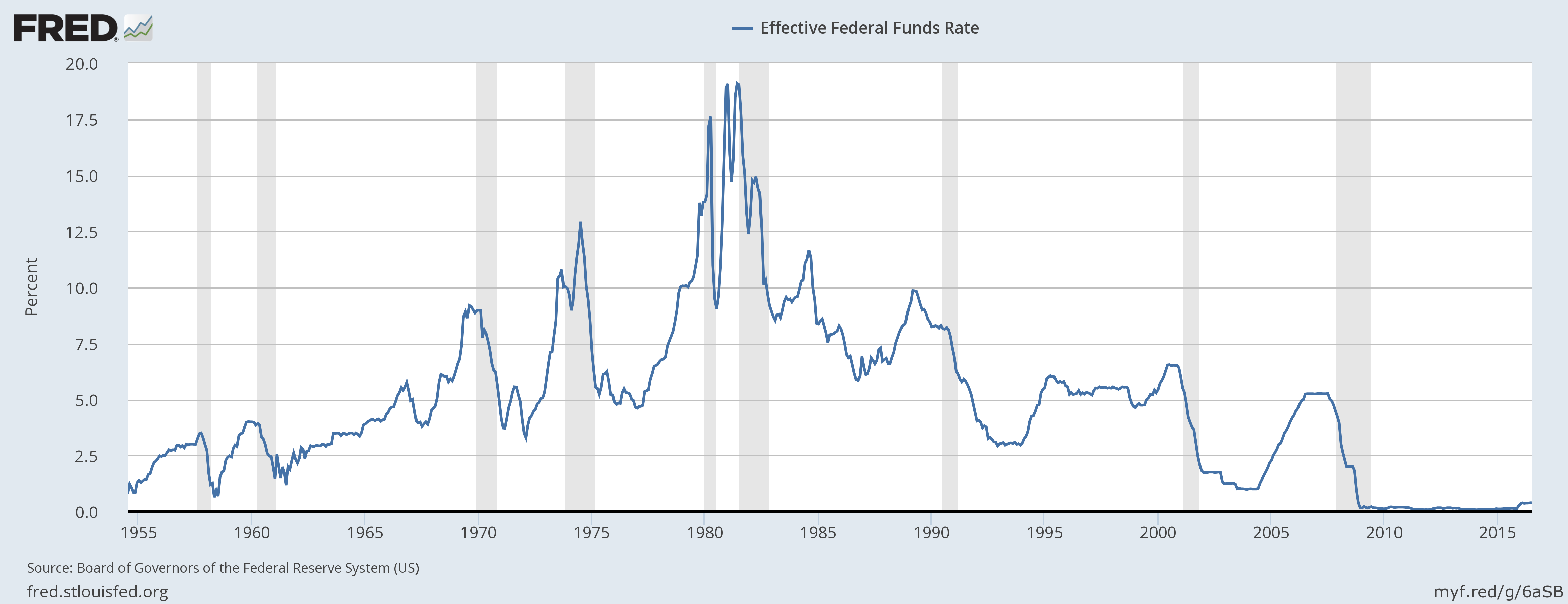

But this raises questions about why interest rates are so low in the first place. As everyone knows, interest rates are historically low because the Fed wants people to spend money and fuel economic growth. Still, many of us can remember times — the 1950s and 1960s — when the economy was expanding and interest rates still held within a normal range. Here is the Federal Funds rate since 1954 posted on Fred.StLouisFed.org this morning:

So, yes, it hit .93 in June 1958. But since December 2008 the Federal rate has never been anywhere near this high; and we have near full employment! So, what gives? Here’s what gives; real wages since April 2006 from this morning’s Bureau of Labor Statistics:

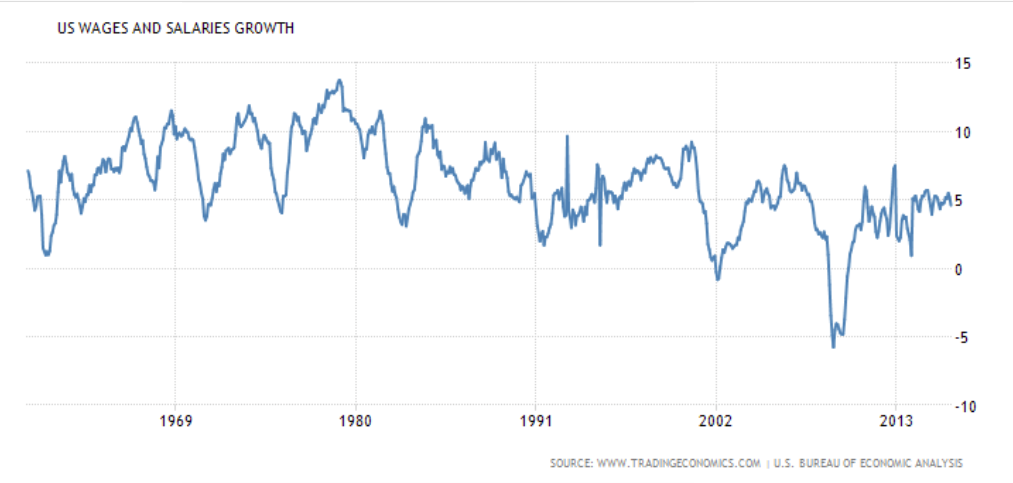

And here is how the Bureau of Economic Analysis reports wage growth since 1960.

Stagnant. Unlike a household budget, the discrete elements within an integrated national economy shape one another profoundly. If I do not maintain the road in front of my house, drivers will either avoid my street or break their axle. To maintain the road we develop equitable formulas whose underlying principle is that when all of our streets are maintained this improves the general welfare of everyone (U.S. Constitution, Preamble).

But when private investors discovered that purchasing policymakers at every level of government was an efficient way to reduce or eliminate their share of public costs, they began throwing huge sums of money into political races. Such sums were justified by the even larger sums of capital private investors saved by shifting public costs onto the shoulders of individuals without sufficient wealth to purchase policymakers. As their share of the public cost increased, working families were told that the fault lay in big government. Reduce the cost of government and working families would (1) receive higher wages and greater benefits from deregulated employers relieved of their tax and regulatory burden; and (2) would enjoy relatively higher wages because their wages would be taxed at a lower level and because products produced by non-taxed, deregulated industries would cost less. Which is the same as saying, when no one pays to maintain the road in front of my house, it will cost less for me to drive on it.

Obviously, since they could earn higher returns in a deregulated environment private investors had no interest in passing their higher earnings either onto workers or onto consumers. The long and short of it is that since 1970, roughly, working families have had to do more with less. Yes, working families are working their tail ends off since the burden of paying for literally everything falls on their shoulders. Thus the historically low unemployment. And, yes, private investors are doing really, really, really well, thank you, since they have been relieved of any responsibility for helping pay for public services. (How well? Compare working families in 1965 to working families in 2016. That’s how well.)

What the Fed Chair should do is tax wealth (my colleague Emmanuel Saez and French economist Thomas Piketty are right). But tax authority does not fall under the Fed. So Ms Yellen has but one tool. And since Congress is completely in the pocket of private investors, it has abdicated all responsibility to use any of the other tools available to public policy makers (other than criticizing big government).

Normally, at full employment, we should raise interest rates. But to mistake our economy for an economy that is overheating is like claiming that I am spending too much because Donald Trump bought another Casino. Investors are doing really, really, really well. But the average working family — the ones who will suffer most from a rate hike — are doing really, really, really badly. And they will do worse with the rate hike. Meanwhile, investors will simply move their capital elsewhere.

Unfortunately, the feeling is that since Ms Yellen is the only adult at home, she should do something. My fear is that she will do what normally would be right, but under the current circumstances is wrong.