I have made no secret of my delight with Yuval Noah Harari’s trilogy. Which is not to say I do not disagree with him at points. For example, it is clear that Harari is finished with the sky gods — Islam, Christianity, and Judaism in particular. I am not there, yet.

Yet. Because there is a sharp disconnect in my own faith, Christianity, between the crucified Palestinian Jew, whom we worship as God, and the cosmic, yet personal, God, the Creator of the universe. There is a sharp disconnect between the son of Mary and Joseph and the Word Who was with God and Who was God.

Harari notes that we all resolve these large or small inconsistencies by embracing and, more importantly, by generating narratives — stories — that round the rough edges, that create logics or syllogisms, which, when placed end to end, make sense of the stories we embrace. Ever since first reading Karl Barth (at Francis Schaeffer’s L’Abri in 1976, shortly before FAS’ passing), I have been inclined to interpret the Cosmic God in terms of the crucified Palestinian Jew, interpreting the impassible through the passible, the infinite through the finite.

This morning during Lauds another thought occurred to me, which could lend itself to a kind of Whiteheadean, process, inflection, but which I do not intend at all in this way. Everything praises . . . God. And then we sing, or chant, all of the things that are praising God. Literally everything. But I was also struck at None that God rules over all things. And I was reflecting (some would say praying) over these Psalms and it suddenly occurred to me that the sheer complexity of the Universe, but also its undeniable order, must give rise to the recognition that we are not in control. What is in control lends itself to a wide variety of narratives. But what is clear is that, we are not in control.

How would I express that we are not in control? Well, Judaism (and, if we trust history, Zoroastrianism before it) said that one (perhaps two) Things, Beings, Forces, Powers were in control.

This is not altogether too far from the scientific truth. Educated people are compelled, I think, to create a narrative that makes sense of this complexity and also the logical, relational, dependencies that extend from the very small to the very large, from the subatomic to the cosmic. We don’t call this logic God. But, if I didn’t know any better, I might call it God. It is All Powerful and, in its own way, All Knowing. And it may even, in a non-humanistic sense, be All Good.

That is the Creator God. That is the God of Romans 1-3. But it is also the Stoic God and the God of the cosmic spiritualities — the apophatic spiritualities, the non-individualist spiritualities. This disembodied, cosmic, spiritualities. Que sera, sera.

And then there is the Palestinian Jew, whose Father, according to tradition, was the Creator God; or, rather, Who was Himself the Creator God.

For me, this invokes a productive self-referentiality. Let us say that the limited, circumstribed, bracketed, Deity, Jesus, is the Cosmic God? Let us say that the hidden, secret wisdom, from the foundation of the world (I Cor. 1-2) is that God is the Palestinian Jew?

And let us say that the oppressive weight of the Cosmic God, or so it often seems, is dissipated in the Palestinian Jew? What I mean is that whatever we mean by God cannot be the impersonal, lawful, logical ineluctable movement from A=>B. What I mean by God is this man, not even Man (capital “M”). This small-case “m,” man. In other words, not humanism. But also not this-human-ism.

The Gospel in this case would not be species-centric. But it would also not be cosmic. It would instead focus intently on relations of power and subservience in and through this narrative. It would be midrash, small “m.” In this case the central tension — Palestinian Jew, cosmic God — is not so much resolved as much as superseded.

“Marx departs from the function of the market. His novelty is the place where he situates labour. It is not that labour is something new but that it is bought, that there is a market of labour. This is what allows Marx to demonstrate what is inaugural in his discourse and what is called surplus-value.”

— The Capitalist Unconscious: Marx and Lacan by Samo Tomsic https://a.co/epSlC3V

Tomšič is quoting from Lacan’s Livre XVI, D’un autre à l’autre:

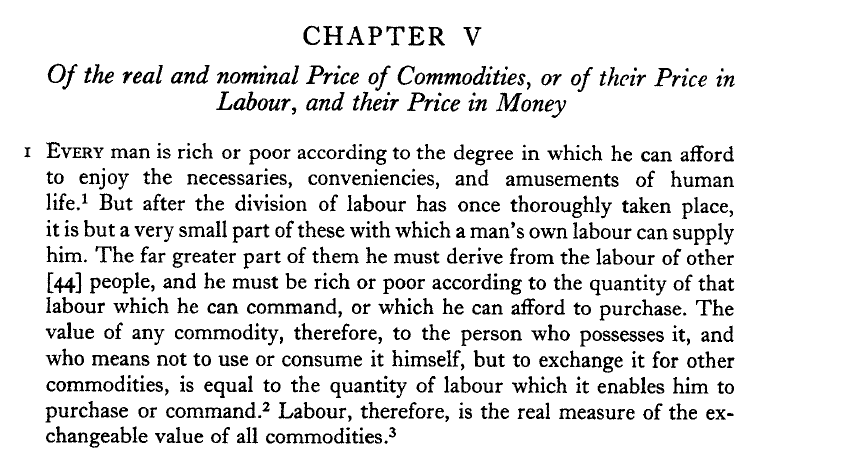

No. In fact this is not new. Nor would anyone — anyone — familiar with classical economic thought mistake it for new. Here, for example, is Adam Smith, Book I, Chapter 5 — the very first paragraph:

Moreover, Smith will proceed in Chapter 8 to show how capital appropriates the surplus-value of labor: “As soon as land becomes private property,” writes Smith, “the landlord demands a share of almost all the produce which the labourer can raise, or collect from it. His rent makes deduction from the produce of the labour which is employed upon land” (I.viii.6).

Marx’s novelty has nothing whatsoever to do with surplus-value or the labor theory of value. Marx’s novelty is to show how social relations under capitalism are mediated by an abstract social form, the value form, that constitutes an historically novel, abstract, logical, subjectively and objectively compelling form of domination.

This should be of interest to Tomšič, since, far better than Lacan, it reinforces his claim that the subject, meaning the human subject, is not autonomous; rather is the abstract value form of the commodity.

I must admit, I have always held some contempt for scholars who suggest something of an eternal conflict between science and religion. One might just as easily or even with more justice say that there is an eternal conflict between science and patriarchy or science and government or science and war and/or peace. For one, when my ancestors were wanderers (and which of our ancestors weren’t?) their very survival depended on a keen grasp of the world around them: weather, seasons, migratory patterns, horticulture, drainage flows, tides, geology. For another, by reducing scientia to only those things that lend themselves to rigorous mathematical modeling — the so-called STEM fields — we in fact severely constrain that can be known, quod non sciatur, to what can be counted, quid est eis numerus. And, yet, I have been wondering why contemporary Christians, Jews, and Muslims who count themselves “traditional” also seem to be enemies of scientia in the broadest sense, knowledge. I have been wondering this even more since reading Maria Rosa Menocal’s Ornament of the world: how Muslims, Jews, and Christians created a culture of tolerance in medieval Spain (2002). Because, contrary to rather unscientific mischaracterizations of the Middle Ages, it was actually only with the dawning of the modern epoch that those who counted themselves “religious” began to dig in their heels. Why? What was at stake?

Let me suggest that at the outset what poses as religious resistance to science can be understood as a misdirected resistance to capitalism. What do I mean? Review the multiple layers of social, cultural, and practical reason that guided social action prior to the birth of capitalism — prior to the fourteenth century — and you will notice how prolific were the logics infallibly guiding communities to happy outcomes. Capitalism invites communities to interpret all human action in terms of its marginal product, in terms of ΔQ/ΔL, where Q is some quantity of, really, anything or no thing, and where L is some amount of labor, although one could also say that it is some quantum of labor-capital, since the two come to be interchangeable. ΔQ is a change in Q relative to ΔL, a change in L. So what looks initially as though it were considering things, is in fact a ratio between two Δs. The rise of capitalism therefore constitutes a dramatic reduction in permissible logics, permissible ways of knowing, permissible things to know. But why could not modern science simply be added, like a Roman god, to the existing pantheon?

This, in fact, is how many conservative, evangelical Christians who happen to be scientists often view their professional lives, in purely formalistic terms. It is not a worldview so much as it is a technique, a minor deity if you will. But this is not at all how modern science — modern scientia — wishes to be viewed. Knowledge is not “in part.” It is not in “a glass darkly.” Should a corner of the universe fall out of the general theory, it immediately attracts scrutiny. Scientists want to know that corner, as it were, “face to face.” If religion “knows” something that science cannot know through the scientific method, then science can do no more or less than ask for a proper scientific demonstration. Short of a proper scientific demonstration — a demonstration proving scientia, proving knowledge — scientists must conclude that whatever it is people religious claim to “know,” it is not scientia, not knowledge.

One way to approach this hubris is to identify, empirically, all of the forms of knowledge — real knowledge — of water flows, migrations, geography, seasons, etc. that science as private industry pushes to the side or eliminates. So, for example, if there is a Creator of the entire Universe, is this Creator truly in a bunch over whether I interpret the first eleven chapters of Genesis “literally,” whatever that means? Or might this Being not be interested in whether I am destroying some small, insignificant corner of Creation called Earth? Does this Creator have an eternal preference for how and which of his creatures give consensual pleasure to one another? Or does this Creator not care infinitely more whether such pleasure-seeking and granting is consensual?

But let us suppose that capitalism has eliminated both the sign-system and the dictionary that might help me grasp what God wants me to do and be? Read the Bible. It was clearly, transparently, spectacularly, written by and for people who farmed and migrated. What is at stake is not whether I can consult a good commentary or Bible reference book. What is at stake is whether I can even read the signs of the times: floods, earthquakes, fires, extinctions, mass migrations, water levels, seasons, etc. Instead, people religious read their Bible, their Talmud, their Koran, as though it were a science textbook. They read them as though they were commenting on sex or biology or astronomy or free trade or democracy or liberty or free will or . . . or . . . whatever. They know that something is terribly wrong. But what?

But, here is what we know. Science is completely incompetent to tell us what questions we should even ask. It is completely incompetent to tell us what we should do. And it is completely incapable of these sorts of things because, at its most basic level, science can be reduced to ΔQ/ΔL. That is to say, it is entirely competent to measure and show relationships, even causal relationships. But it is completely incapable of telling us why they are important.

People religious know — or, in any case, they suspect — that science does not know these things. And they suspect that science is responsible posing as an answer to these questions. “Well,” people religious say, “I have an answer. It’s in the . . .” Bible, Talmud, Koran . . .

Resistance to science as resistance to capitalism.

But what if we now replace the marginal product with the widest possible variety of ways of grasping our world: aesthetic, ecological, geographic, topographic, stratospheric, planetary, archeological, agricultural, sociological, psychological. That is to say, what if our lives with one another are actually mediated by the stories we tell about these different formations and about the empirical, practical, tests we perform to verify these stories. What if we liberate these spheres from their bondage to ΔQ/ΔL?

In that case we might have to revisit the Islamic Mediterranean of the Middle Ages.

“for Marx there is no subject of surplus-value, unless one fetishises the appearance of capital as the vital subject of valorisation, as is the case in the developed forms of capitalist abstractions such as financial capital (but also on the more ‘immediate’ level of commodities and money).”

— The Capitalist Unconscious: Marx and Lacan by Samo Tomsic

https://a.co/1M9iQsl

This is simply mistaken. Either Tomšič is unfamiliar with the Marx passage on the Subject, which is doubtful, or he is unfamiliar with its source, again doubtful, or he has never put the two together, more likely.

The Marx passage:

It is constantly changing from one form into the other, without becoming lost in this movement; it thus becomes transformed into an automatic subject. If we pin down the specific forms of appearance assumed in turn by self-valorizing value in the course of its life, we reach the following elucidation: capital is money, capital is commodities. In truth, however, value is here the subject of a process in which, while constantly assuming the form in turn of money and commodities, it changes its own magnitude, throws off surplus-value from itself considered as original value, and thus valorizes itself independently. . . . But now, in the circulation M-C-M´, value suddenly presents itself as a self-moving substance which passes through a process of its own, and for which commodities and money are both mere forms. But there is more to come: instead of simply representing the relations of commodities, it now enters into a private relationship with itself, as it were (Capital, I.iv).

Marx is not fetishizing the value form of capital. Rather is he disavowing (1) that the subjects to the exchange are subjects; (2) that the surface form of appearance, “the commodity,” is subject; and (3) that the money form is subject. It is instead the value form of capital that is subject, not “labor-power” as Milner and Tomšič suggest and perhaps Lacan implies. Marx here historicizes and socializes Hegel’s grasp of the Subject from Phenomenology:

Further, the living Substance is being which is in truth Subject, or, what is the same, is in truth actual only in so far as it is the movement of positing itself, or is the mediation of its self-othering with itself. This Substance is, as Subject, pure, simple negativity, and is for this very reason the bifurcation of the simple; it is the doubling which sets up opposition, and then again the negation of this indifferent diversity and of its antithesis [the immediate simplicity]. Only this self-restoring Same-ness, or this reflection in otherness within itself — not an original or immediate unity as such — is the True. It is the process of its own becoming, the circle that presupposes its end as its goal, having its end also as its beginning; and only by being worked out to its end, is it actual. Thus the life of God and divine cognition may well be spoken of as a disporting of Love with itself; but this idea sinks into mere edification, and even insipidity, if it lacks the seriousness, the suffering, the patience, and the labor of the negative (Phenomenology §§18-19).

This is not a feature of language, not of signifier and signified, but of the commodity, both its value form and its surface forms of appearance.

In chapter six of their Principles, Krugman and Wells explain demand price and supply price elasticity. Intuitively, elasticity makes sense. A good that everyone needs (e.g., petrol, water, oxygen, health, food), regardless of price, will be demand price inelastic. A good that will be supplied in the same volume (e.g., nuclear warheads, grapes, PPE), regardless of price, is perfectly supply price inelastic. (How much are you going to pay for a nuclear warhead? If you want a nuclear warhead, you will pay . . . whatever.) In the long run, producers might shift cultivation from grapes to cannabis, but a change in price will not alter the volume of one or the other or both that a cultivator will supply. Only under highly unusual circumstances will a community elect not to supply its members with sufficient protective equipment to mitigate the spread of contagion, irrespective of price.

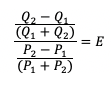

Again, what is perhaps most significant about elasticity is how accurately our neoclassical model captures actual market behavior. That is to say, what is remarkable is that human conduct lends itself to rigorous mathematical modeling. In particular:

Where Q2 is the quantity of a good demanded following a change in price and Q1 is the initial price; and where P2 is the price corresponding to the quantity demanded following the price change and P1 is the initial price. In elasticity, again, consumers are not responding to the substances out of which things are composed. They are instead responding to a correlation between their need (however measured) and price — price, however, not as the cost of any thing out of which a good is composed, but as a multivariate calculation of their need measured against the needs and prices of all possible goods. Where E > 1 demand is elastic, i.e., it is responsive to price; where E < 1 demand is not elastic to price; and where E = 1, demand is unit elastic.

From which it follows that price elasticity is not only a factor of my “need,” but also the substitutes that might also satisfy this “need,” whether I judge the good a necessity or a luxury, but also, therefore, the elasticities of substitutes.

Consider the condition where a consumer is at risk purchasing food — often deemed a necessity — in her own neighborhood. Industry and high wage/high benefit employment left her neighborhood a long time ago, when the mines closed, when the factory moved off-shore, when manufacturing proved too expensive because healthcare costs are privately funded, when property prices declined, when policing turned against the residents, when the public elected not to fund schools, repair roads, maintain utilities . . . Consumers are at differential risks leaving their homes. They are also at risk entering other neighborhoods where the price of food might be less. For a variety of reasons, a consumer decides there is a higher marginal cost shopping outside her neighborhood. To this risk we might add opportunity cost. If we drives or takes mass transit to another neighborhood where prices are lower, the time and effort it takes her to travel, plus the risk, makes shopping locally relatively more attractive. But it also makes her behavior less price elastic. She will be willing to endure higher prices. Again, the question here is not whether “objectively” the higher prices she is ready to pay are offset by travel time and risk. The market, in aggregate, suggests that she will be ready to pay considerably higher prices for goods for which other consumers elsewhere pay less.

But, elasticity also tells us something about income. When a consumer is not constrained by income, price is less elastic; that is to say, consumers who enjoy more wealth than they need are less influenced by price changes than are consumers who must make decisions over whether to buy food or medicine, diapers or books, Internet or clothing.

For consumers who fall in the latter group, income elasticity shows up in the kinds of goods they purchase. Inferior goods are goods that sell in greater quantities when income drops. Normally, goods have a positive income elasticity. As income increases, consumers will purchase more of them. Inferior goods by contrast become more attractive when incomes fall.

Once again, Marx would entertain few objections to Krugman and Wells’ treatment. We can imagine conditions under which families do not have to choose between food or medicine. But we cannot imagine conditions in capitalist societies where price elasticity cannot be calculated or modeled and therefore where producers take consumer behavior as a signal for whether to produce more or less of some good. For example, we notice that when oil reserves plunge, prices climb. But, let us suppose that reserves climb. Since the price of petrol is relatively demand inelastic — i.e., since consumers will have to drive irrespective of the price — prices will never fall in line with supply.

For anyone therefore who thought that price or value were somehow hardwired into things, price elasticity or inelasticity should be enough to convince them otherwise.

In chapter five of their Principles of Economics, a chapter subtitled “meddling with markets,” Krugman and Wells look at price controls and quotas. To repeat, my aim in this series is not to disclose an occult Marxian way to pursue economics, but rather to show how Marx was in nearly all respects a fairly straightforward neoclassical economic thinker. The matter of price controls and quotas is a case in point. Insofar as commodity production and exchange aim to produce and expand value, any intervention into production or exchange that impairs or impedes this production or expansion in order to achieve some end other than production and expansion is, by definition, an impediment to market efficiency.

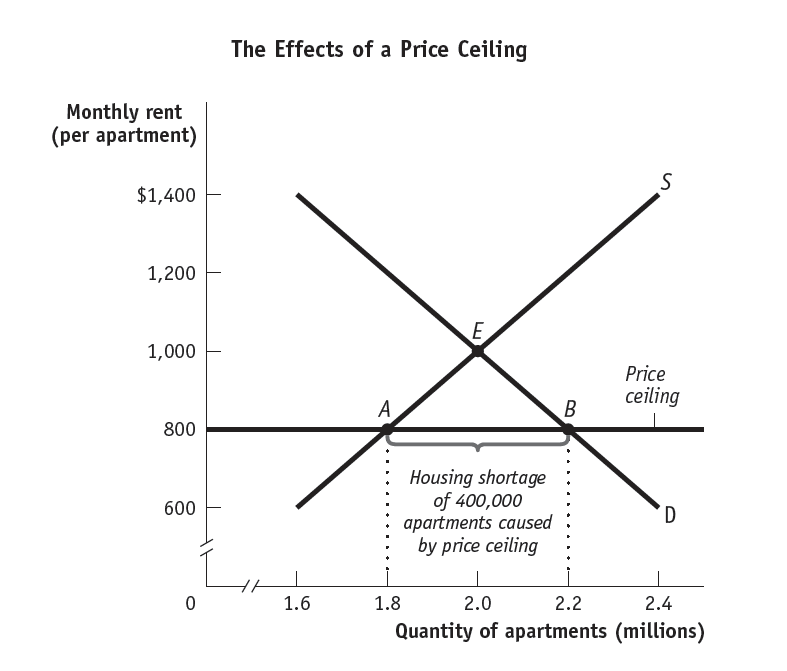

So, for example, some entity might wish to make rents more affordable and to this end might place a ceiling on what property owners can charge renters to let rooms, apartments, or homes.

In this example, where property owners could charge $1000 per unit, they would place 2M units on the market, where supply and demand intersect (E). Should an entity limit to $800 per unit the price property owners could charge, demand for $800 units would increase to 2.2M, but property owners would, at that price, only be willing to place 1.8M units on the market, giving rise to 200K fewer units than would have been let at market price (E) and 400K fewer units than were demanded at the rent-controlled price.

Economists call the shortfall “deadweight loss.” They call the lag in supply an “inefficient allocation to consumers.” Moreover, since producers will take units off the market that might otherwise be available, and since consumers will be compelled to seek alternative housing, resources will be wasted. Also, the units that property owners will be willing to place on the market will hold values no greater than $800. You get what you pay for.

But let us say that your professor has an in-law unit she is willing to rent to you for $1200 “off the books.” Price ceilings also therefore give rise to so-called “black markets.”

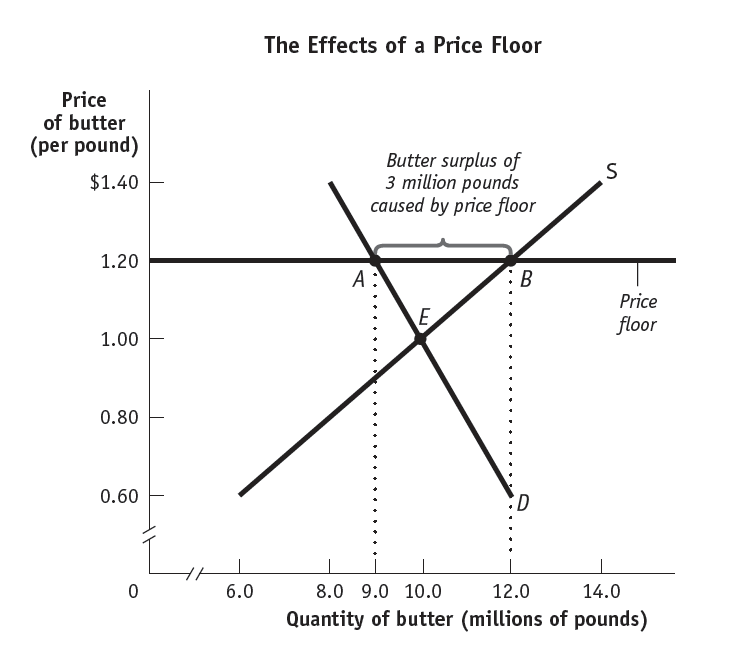

Price floors have a similar effect on markets. Let us say, for example, that more consumers would purchase a good were its price permitted to fall to equilibrium, but that fewer producers would be willing to produce a good at its equilibrium price:

At equilibrium, therefore, producers produce only 10M lbs of butter when butter is only $1/lb. Yet, should some entity fix a lower boundary on what producers can charge, in this case $1.20/lb, producers will be willing to produce more butter, 2M lbs more butter, but consumers will demand 1M lbs less butter than they would at equilibrium, and will demand 3M lbs less butter at $1.20 than producers are willing to supply at that price.

Once again, the effect will be deadweight loss, since the quantity bought and sold will be lower than it otherwise would be; an inefficient allocation of sales, since producers will be deterred from entering a market where demand has declined; and unnecessarily high quality will prevail, since consumers would otherwise be willing to pay less for a lower quality of good. And, just as in price ceilings, so price floors give rise to illegal activity.

Where price floors and ceilings make use of the price mechanism, quotas make use of quantities. Krugman and Wells illustrate the effect quotas have on markets by showing what happens when a city limits the number of taxis that can operate on its streets. (New Yorkers must bear quietly with this example.)

At equilibrium 10M riders would be willing to hail cabs for fares of $5/ride. By limiting the number of cabs available for hire to 8M, the regulatory authority has selected a point on the supply curve that suggests a fare of $4/ride. But, in fact, with the dearth of cabs, riders are now willing to pay $6/ride, a dollar more than equilibrium, which is good for all of those able to afford a medallion. The “wedge” indicates the “rent” riders pay for the limit placed on number of cab drivers. But, let us say that I find a cab driver operating outside of the law. And let us say that she will charge me $5/ride until she learns that I am with the regulatory agency, at which point she drops the fare even further. Or take another example.

Land owners in the Central Valley of California are always eager to drive down wages for seasonal agricultural workers. One way to drive down wages would be to open the border between Mexico and the US to workers who, generally, are willing to accept a lower wage than domestic laborers. (This, for example, is how Germany has solved its shortage of healthcare and waste management workers.) But, since legal workers in the US enjoy greater protections than workers in Mexico, Central Valley land owners would have to compensate migrant seasonal laborers from Mexico at a much higher wage than they are willing to pay. Placing a strict quota on documented workers would appear then to deprive Mexican migrant laborers who are willing to work access to employment and deprive Central Valley land owners laborers to work their farms. But, let us now say that regulators turn a blind eye to land owners who hire undocumented workers; and let us say that land owners deprive undocumented workers legal protections in exchange for allowing them to work. In this case, quotas that are selectively enforced can create what has been called the $1.25 apple. Normally, were workers paid a living wage, that same apple would cost $25 — providing an incentive for growers to mechanize their industry. As it is, absent a wage floor, consumers get the best of both worlds: an affordable apple.

Here again, Marx would find little to dispute in Krugman and Wells’ analysis. Insofar as social relations in capitalist societies are mediated by the production and exchange of commodities, goods are produced not in order to satisfy desire for goods, but in order to satisfy desire for abstract value. Where the marginal product has been limited by any external constraint — a price floor, price ceiling, or quota — producers and consumers are compelled to compensate for their loss by making other choices. So, for example, in the case where immigration from Mexico is legally constrained, growers wishing neither to mechanize their production nor charge $25 per apple are instead forced to find ways around the law. Your professor is forced to rent out her in-law unit beyond the reach of regulatory authorities. And medallion owners trade in medallions priced at several years’ income.

Where Marx would object is in the conceit that markets are ever unconstrained. In order to function at all, markets always operate under constraints. As the above examples illustrate, value is no law-abiding citizen. It is always in search of the shortest distance between two points, the law notwithstanding. The question, therefore, is (1) how will policy makers and enforcers select the constraints that constrain markets; and (2) who will bear the cost of the inefficiencies generated by these constraints?

Consider the case of rent control. By holding rents down, there is greater demand than private owners are willing to supply. But let us then suppose that the producer of some good — a university for example — nevertheless gains value from a steady and growing supply of tuition-paying-units. Or, more generously, let us say that a state — California for example — finds value in a highly educated and innovative workforce. In that case, either of these entities should be willing up to the margin, to make up for the deadweight loss arising from rent control. Or, in the alternative, California could highly subsidize public higher education in general, allowing institutions such as UC Berkeley, to offer a four-year education for free, making more disposable income available for other uses, such as rent. Or, both of these entities could coordinate their efforts in any number of ways. But why?

In Marx’s view, the only reason any of these entities would take any of these steps would be to increase the value of their marginal product. In no case would they elect to do so should it flatten or depress their marginal product. Public health and education increase aggregate marginal value. Yes. Of course. Which means that they pose no threat to the capitalist social formation.

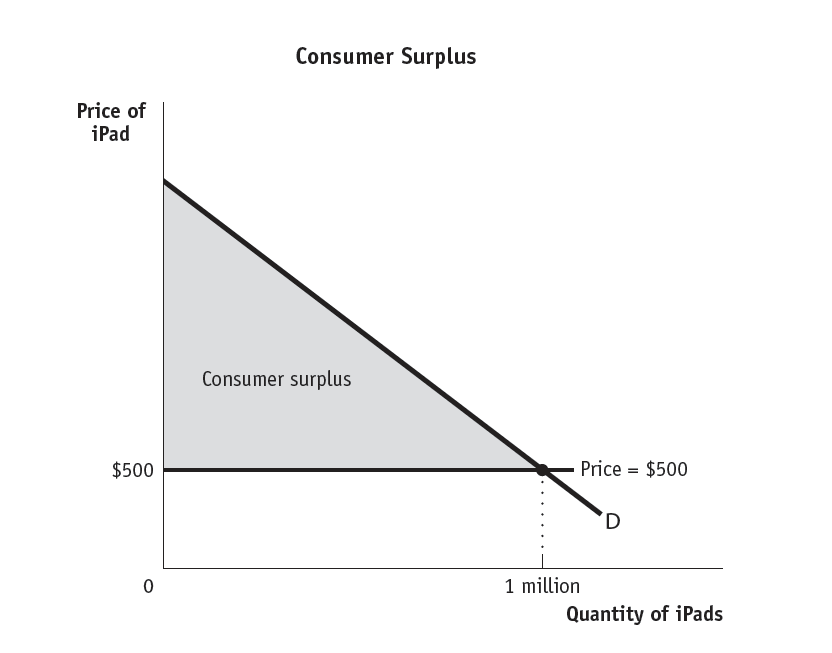

In chapter 4 of their Principles of Economics, Krugman and Wells take up Consumer and Producer Surplus.

Consumers almost never pay the full price they would be willing to pay for a good. This follows from the fact that producers distribute goods and retailers price goods to attract not all potential consumers irrespective of their individual disposable income or desire for the good, but the optimum number of buyers at a specific price. Some buyers would be willing to pay substantially more. For some buyers, the retail price will be too great. The consumer surplus measures the value of a good for which consumers did not pay in aggregate.

It stands to reason that, as retailers price goods closer to their cost, this will increase the number of consumers eager to purchase those goods.

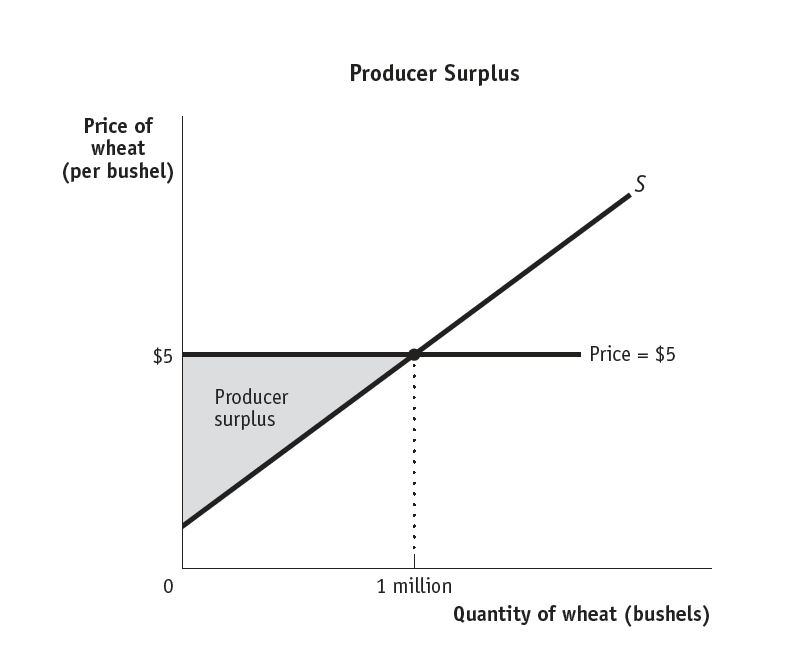

The same holds true for producers. Producers could sell a good at cost. As they increase the price they charge to retailers for a good, this will, by definition, decrease consumer demand. But producers rarely sell a good at cost. Producer surplus in aggregate equals the sum of the differences between cost and price.

It follows that as the price at which producers can sell a good increases, producers will produce more of that good. As the price declines, producers will produce fewer items.

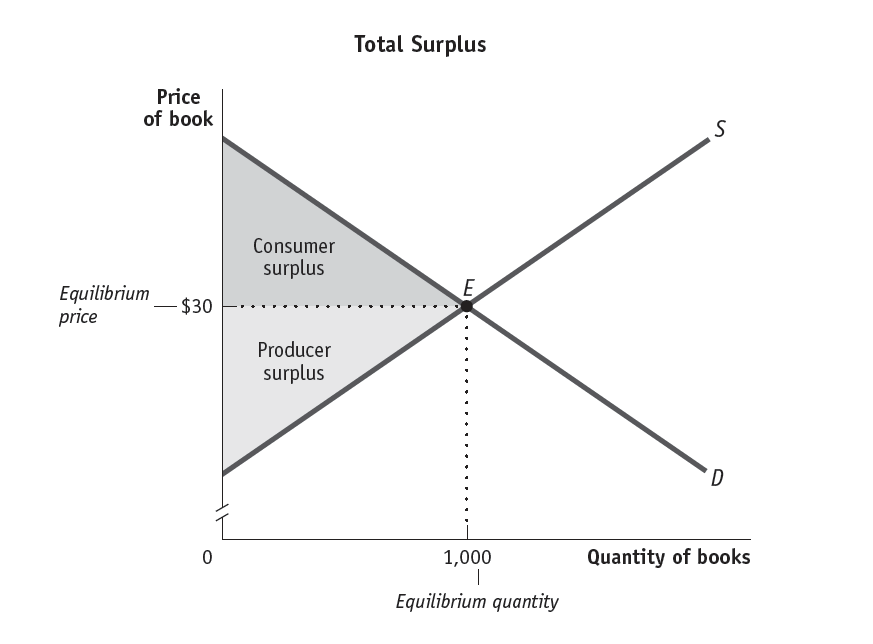

Total surplus falls where consumer surplus and producer surplus intersect:

But, again, we must emphasize that the triangles above and below equilibrium price are not evidence of exploitation. They are evidence rather of the abstract, immaterial character of value: value is not a quality in the substances out of which things are composed. Value is the abstract social substance that mediates social relations, i.e., in this instance, the social substance that induces publishers to print and distribute books and induces buyers to purchase them.

Equilibrium price is above the cost producers bear to produce books; equilibrium price is below the price consumers would pay for books. The area in both the triangles combined measures the total surplus or value won in aggregate by consumers and producers.

Krugman and Wells tell us that equilibrium price “allocates the good to potential buyers who value it the most” and “allocates sales to potential sellers who value the right to sell the good the most.” This requires some clarification. “Value” in this context needs to be understood as “value in the abstract.” Although, the meaning (sometimes deliberately, sometimes inadvertently) is ambiguous, value is, by definition, not a subjective quality of either buyer or seller. Thus, as Krugman and Wells note, an efficient market is not the same thing as a “fair” market; moreover, efficient markets do not please all consumers and producers all the time — by definition.

Krugman and Wells conclude the chapter by giving greater definition to market economies. Market economies are economies that grants an entity — public or private it makes no difference — the right to sell a good. So, for example, a public utility has the right to sell electricity (or water or gas, etc.). Producers and consumers rely upon signals — principally price — to help them make informed decisions.

Here Krugman and Wells discuss two concepts that require special attention: inefficient markets and market failure. Markets behave inefficiently when decisions to produce or consume are based on less than adequate signals to inform their decisions. So, for example, when central planners under “market socialism” decide how much bread to produce, the demand for bread at market price provides a less than adequate signal for determining how much bread to bake because the price is calibrated to the incomes of consumers and because the resources for baking bread are calibrated not to the cost of production but to the demand for bread. Value, under such circumstances, is subjected to substantive needs and conditions. Under normal circumstances, needs and conditions are subject to value.

Market failure is a much more problematic concept. So, for example, would we say that the market failed in 1929? Assets in 1928 adequately reflected what producers were willing to produce at prices consumers were willing to pay. Then in 1929 these assets lost considerable value because producers were unwilling to produce goods at prices consumers were willing to pay. The signals in both cases were clear. Consumers and producers relied in both cases on these signals. Insofar as this holds true, it is difficult to call 1929, the Crash, a market failure. The market “failed” only in one sense. The surface forms of appearance, the substances people wanted and needed, could not be procured at any price because the cost of producing these goods at any price exceeded the price consumers could pay. But, again, in what sense is this a “market failure”?

Krugman and Wells define market failure: “when a market fails to be efficient.” But is this really helpful? When producers stop producing a good — bread or PPE — because they cannot produce it efficiently, is this not instead evidence that markets work precisely as neoclassical economists predict they should?

Marx would fiercely dispute the notion that hunger, high unemployment, destitution, social unrest, or market turbulence provide evidence of market inefficiency or failure. Rather are they evidence that markets are performing precisely as they should perform.

But, what if public entities intervene to regulate production and consumption, let us say by heavily subsidizing the production of PPE or by providing universal, single-payer healthcare? There are two ways to think about public financing and regulation of production and consumption:

(1) by definition, they will place upward pressure on price. So, for example, when public entities elect to make war and provide funding to producers, public or private, to produce weapons and provide logistics, the RFP will infallibly place upward pressure on the price of the kinds of goods weapons and logistics producers provide and war-making publics consume. Regulation of prices and public oversight of production may help to keep prices lower than they would otherwise be. But, to the extent that war poses an existential threat, producers will likely push the marginal value of their goods in the direction of ∞, the value of all of the lives of citizens in a nation. But — and this is critical — public funding and regulation generate inefficiencies only because and insofar as they confirm the validity of the underlying market principles; and, so,

(2) we might also think about public funding and regulation along the lines (a) of any insurance scheme, whose costs decline in direct proportion to the range and volume of those covered; or (b) any public good, such as police or fire protection, whose value to all those covered declines as the proportion of covered to non-covered declines. In both of these cases, a greater efficiency is felt to arise from the inefficiencies accepted in a single sector or market. So, for example, free public education and training that extends from universities and trade schools to graduate studies spreads out the cost of a skilled and educated workforce throughout the entire population. It also dramatically increases the pool of highly skilled and educated workers from which employers, public and private, can choose, thus placing downward pressure on the wages any prospective employee can command or employer will offer; but since the work performed will be skilled, it raises the aggregate wages and benefits. The same obviously holds true for other public goods.

Neither of these instances requires that we adopt a different set of economic principles. Nor would Marx fault these principles for inadequately grasping how the capitalist social formation works. He would only object to Krugman and Wells’ definition of “market failure.”

In Chapter 3 of Principles, Krugman and Wells introduce supply and demand. The supply and demand model is premised on a competitive market. Krugman and Wells first illustrate the demand curve; they then examine the supply curve; they then put the two together to locate market equilibrium; and lastly they examine what happens when the supply or demand curves shift and when both shift simultaneously.

To repeat, my aim is not to lay out all that Krugman and Wells have to say or all that Marx might say in response. My aim is simply to show that Marx was a fairly unremarkable neoclassical economic thinker. His contribution to economic thinking rests in his showing how economic action in fully elaborated capitalist societies is socially and historically embedded. Economic actors behave as they do in capitalist societies not because it is “in their nature” so to act. There is too much history, 2.4M years, that says otherwise. They behave as they do in capitalist societies because their social relations are mediated by the two-fold form of the commodity. The commodity’s two forms — its abstract value form and its material form of appearance — shape but are in tension with one another. They are not identical. This mutually constitutive relationship within the commodity is what lends to capitalist society its dialectical, dynamic, progressive form. In neoclassical terms, since the value of a commodity is subject to aggregate supply and demand prices, and since producers can increase/decrease the values of commodities in any number of ways without changing the commodity’s surface form of appearance, there is an abstract compulsion within capitalism to produce more with less: there is a compulsion to increase ΔQ/ΔL.

Demand seems like a transhistorical, universal phenomena. It is. What is novel is that demand is subject to a form of value that is specific neither to the substances out of which a good is composed nor to the specific labor by which it is composed. It is subject instead to the differential values of all goods and all labor and demand for both within a comprehensive, integrated market (see 2/32).

Supply and demand are distorted whenever they are constrained by non-market forces. So, for example, an entity that enjoys a monopoly over a good or factor of production does not necessarily undermine the principles of supply and demand since that entity is not free to set a price on that good above the price that consumers are willing and able to pay. Should that entity set a price for the good above “market price” that entity will, by definition, begin to see a decline in demand. If, on the other hand, an entity is able to compel consumers to purchase its good irrespective of price, this would constitute a market distortion. When a cable company is the only company offering Internet in an area, and when Internet is necessary for conducting business, that company introduces a distortion into the market. “A competitive market is one in which there are many buyers and sellers of a good.”

It is important that we notice that markets permit distortions, some of them quite significant, all of the time. So, for example, fire, police, utilities, and public safety constitute huge market distortions tolerated in even the freest of free markets. It could be argued that they give rise to efficiencies elsewhere in other markets for other goods. But this does not mitigate their own distorted character. What is their supply price? We may never know.

Assuming a reasonably competitive market, Krugman and Wells represent the demand schedule and demand curve as follows:

There is nothing specially noteworthy about the demand curve except perhaps to notice that it calibrates a surface form of appearance, coffee beans, to a value that presumably is not stamped on each or all of the beans. Their value is not the same as, but is nevertheless related to, their substance or surface form of appearance. But, as Krugman and Wells point out, their values are also related to differential valuations of other goods and changes in production elsewhere in the market that have nothing to do with this surface form of appearance.

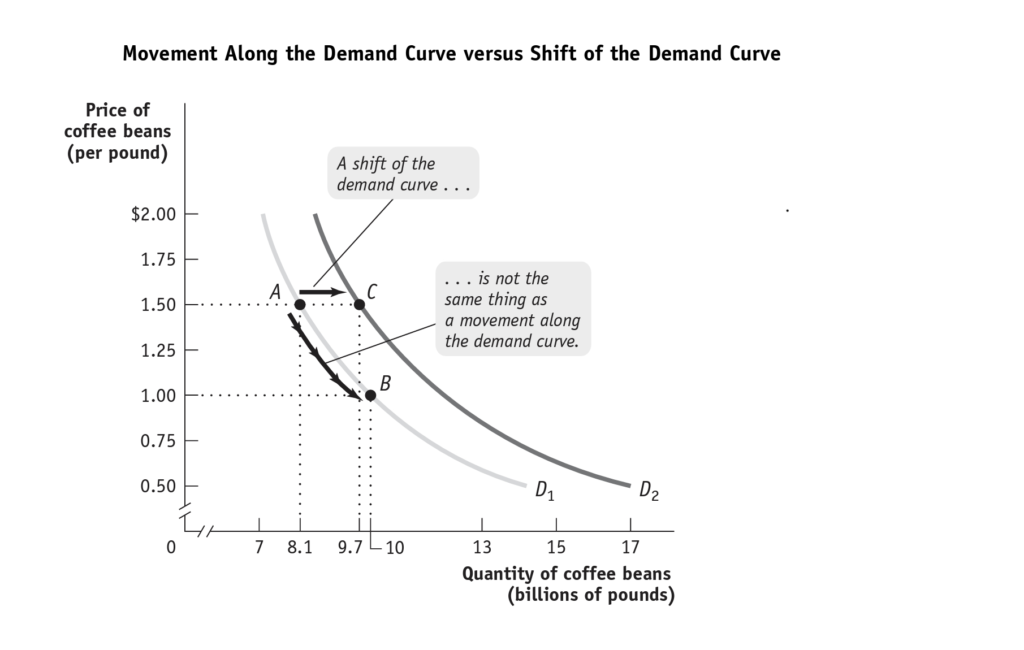

Krugman and Wells then point out the difference between a shift along the curve and a shift of the entire curve:

We can imagine any number of reasons why beans might become more or less expensive. And we can imagine any number of reasons why, at any price, people might choose to purchase more beans. And we can imagine any number of reasons why at the same price, consumers might purchase a higher quantity.

What needs to be noticed is that all of the reasons Krugman and Wells suggest are in line with Marx’s analysis, i.e., they are not uniquely “Marxian.” For example, the value of a substitute good falls while another rises. If the values of two complementary goods rise (or fall). Income of consumers in aggregate may rise. If the value of a good falls as incomes rise, we call that good “inferior.” Tastes change. Expectations change. The market grows.

In all of these cases we have not to do with the substances out of which things are composed, but their differential values relative to one another. That is to say, the values of goods are socially mediated.

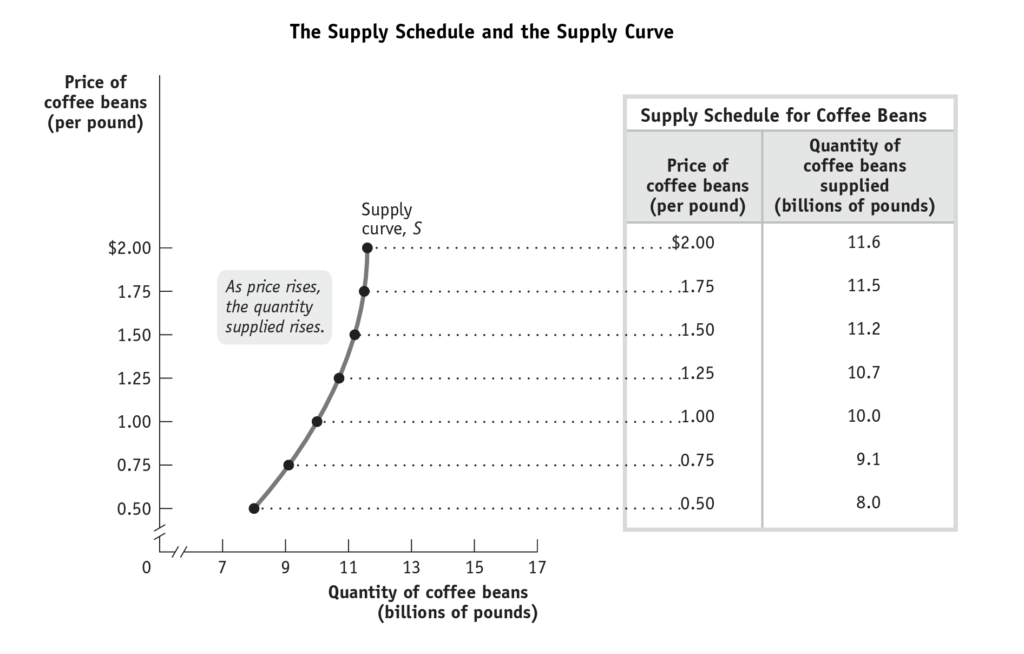

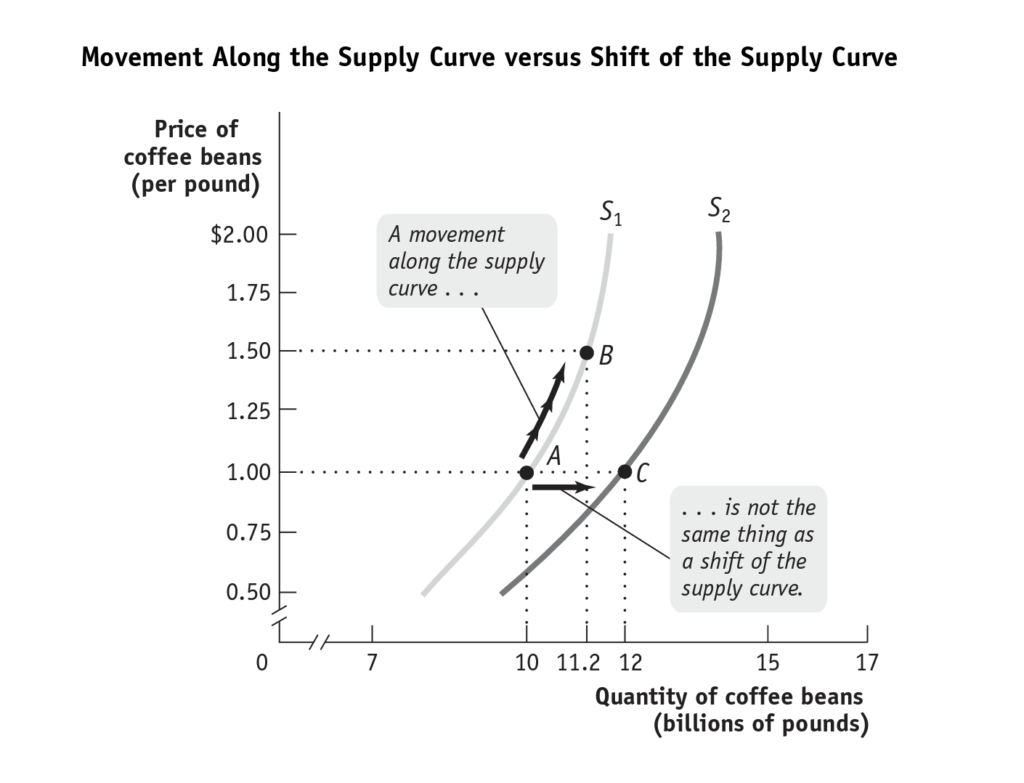

But the same also holds true for the supply curve:

The supply price is in no manner related to my desire for beans. It is related to aggregate desire for beans. Aggregate desire for beans, in turn, is differentially correlated to the values of other competing and complementary goods. But, again, we can imagine any number of reasons why, along the curve, producers might be willing to produce more or less at a greater or lower cost.

And these reasons have little to do with the substances out of which beans are composed or the desire consumers express for these goods. Similarly, we can imagine any number of circumstances under which producers would be able to produce more for less, circumstances that leave the substances of beans or the satisfaction consumers derive from beans unchanged.

What needs to be noted is not that need or desire remain constant; or that the substances out of which beans are composed remain constant. What needs to be noted is that desire and need can be mapped infallibly without the least need to consult the desire or need of consumers or producers. In an integrated multivariate map of goods and values, any individual consumer’s or producer’s subjective need or desire is buried beneath the aggregate. The sole aim of the aggregate is to increase the MPL or MPC, the marginal product of labor or the marginal product of capital.

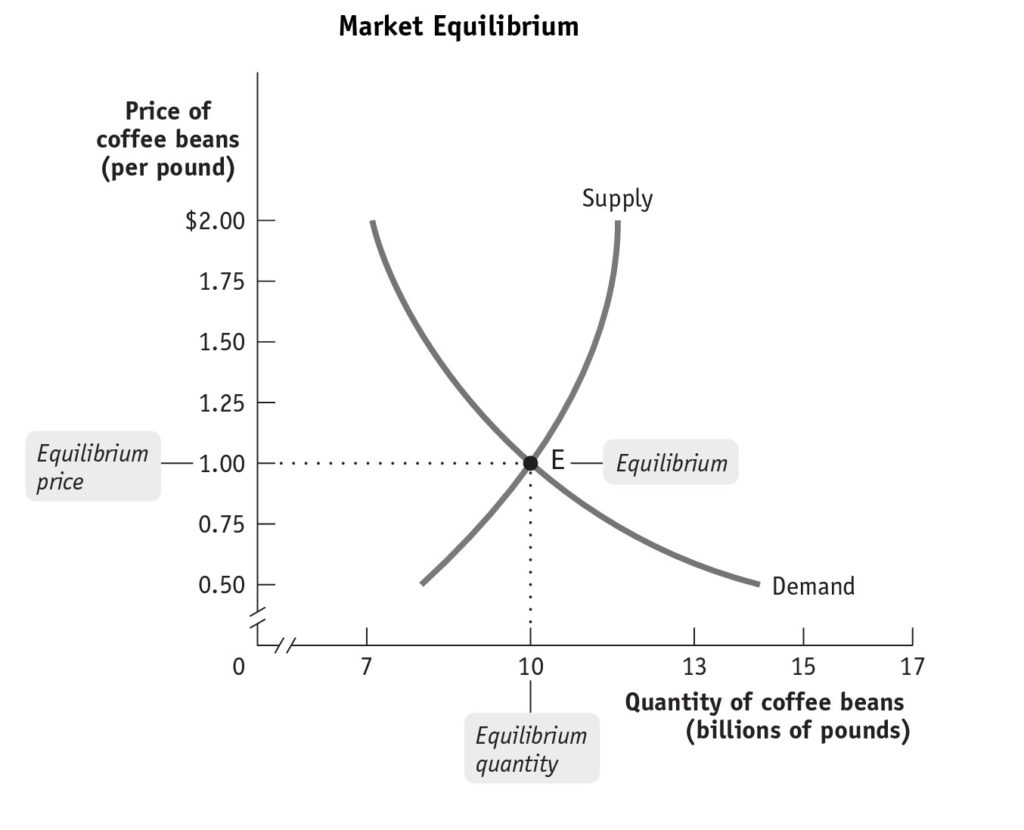

Obviously supply and demand intersect. Optimally, they intersect where all consumers who want a good obtain it and where all producers who produce a good find a consumer willing to produce it at the price they can afford. The illusion of neoclassical economics, which Marx shared, but by which he was not fooled, is that this is always already the constant, ever-present, condition of the market. But this only holds true, of course, in aggregate. Households there are many that want affordable healthcare. But since the value and price of healthcare is generated in aggregate, the equilibrium price of healthcare will be well within the means — a mere drop in the bucket, pocket change — for some families, while it will be completely out of reach of others. Nevertheless, the equilibrium price — the equilibrium supply and demand at a price — of healthcare will be infallibly generated by the market.

If it is not already clear, then by now it must be. Krugman and Wells are illustrating their point with price of coffee beans and quantity of coffee beans. But we could be talking about anything, or nothing. We are talking about value and its surface form of appearance, in this case beans.

Obviously Krugman and Wells have much more to teach us. But they have already taught us about as much as we need to know. In the capitalist social formation, you are powerless. In the capitalist social formation, aggregate supply and aggregate demand are everything. But supply and demand themselves are not for things. Supply and demand are for values, which are constantly shifting both along the curve and with the curve, both of which shift for reasons entirely independent from the substances out of which things are composed.

More importantly, consumer desire shifts irrespective of these substances, irrespective of these surface forms of appearance.

Krugman and Wells do not dispute these points. They illuminate them. Neoclassical economic thinking is not anti-Marxist. It is agnostic. It is simply providing tools for characterizing economic behavior. Marx wished to show how the principles of neoclassical economic thought themselves showed why capitalism was not inherently emancipatory. It is not.

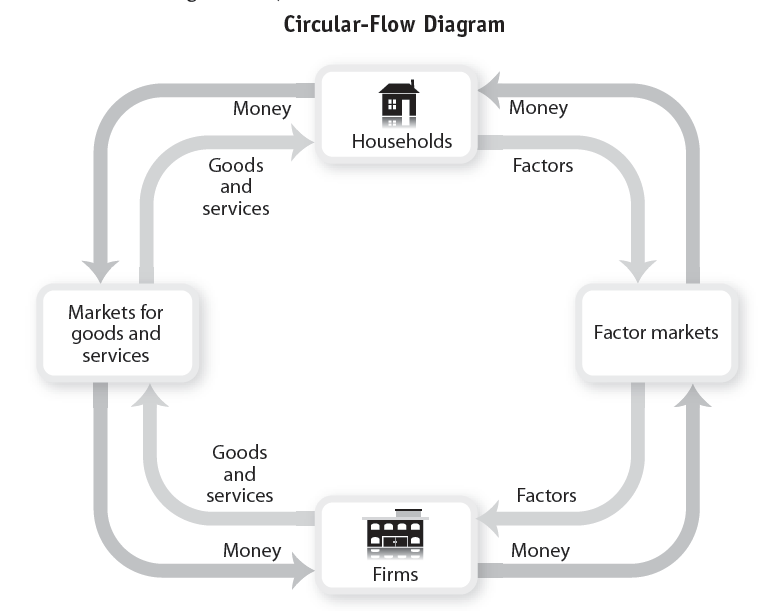

In chapter 2 of their Principles of Economics, Krugman and Wells introduce trade-offs and trade. The chapter is divided into five sections: (1) introduces the concepts of modeling and caeteris paribus (all things being equal); (2) looks at the production possibility frontier, which identifies how producers decide what they should produce; (3) looks at comparative advantage or why all parties to trade can come out ahead; (4) looks at what is called the “circular-flow” diagram:

And lastly (5) which aims to distinguish between positive and normative economics. There is also a sixth section, which deserves separate treatment: when and why economists disagree.

As I mentioned in 1/32, so long as we remember that we should not be able to model human action using rigorous mathematical modeling, nothing would prevent or did prevent Marx from agreeing that human action in fully developed capitalist economies does lend itself to rigorous mathematical modeling. Caeteris paribus is also unnoteworthy. It simply shows that we are always selecting variables that we feel will most faithfully answer the question we are asking. We do not throw all existing variables at each question. Rather, we assume that all other things are equal.

To be sure, this can prove problematic, as when an economist assumes that wealthier individuals “prefer” better health, housing, and education than poorer individuals, since wealthier individuals “choose” better health, housing, and education than poorer individuals. Under such circumstances caeteris non paribus. Once we include systemic racism, institutional discrimination, and the “differential values” placed on different segments of the population, we will then discover that some of the variables left out of the model actually turn out to be critical. But the fault is not in caeteris paribus as a principle. The fault lies with researchers who exclude critical variables, or, more to the point, societies that value individuals differentially.

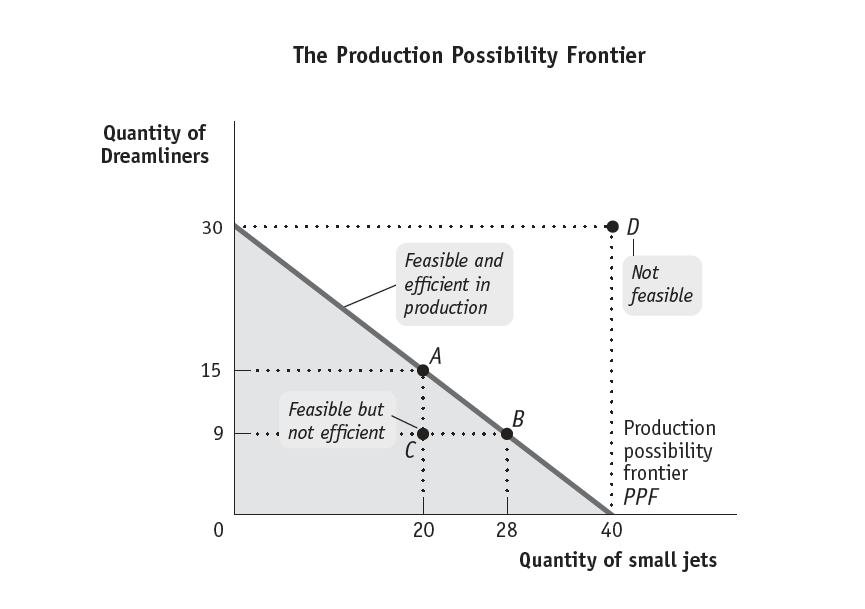

Nor would Marx, in principle, have problems with section two. In the simple model introduced by Krugman and Wells, we are invited to consider only two goods, Dreamliners (yes, no kidding) and small jets.

Since we cannot produce everything, there is some relationship between small and large jets. We could produce fewer of both (C), in which case we would lose six dreamliners we could have produced and eight small jets we could have produced. But we cannot under any circumstances produce 30 dreamliners and 40 small jets. Why? Because there are insufficient resources. Or, more specifically, because acquisition of sufficient resources would itself be inefficient. Why? Because available resources are measured in terms of the abstract value investors are willing to part with in order to develop a resource. Available resources are assumed constant in this model.

But let us suppose that investors invest in a technology whose cost proves lower than the value this technology earns by developing more resources? In effect, this new technology decreases the cost of developing a resource making it available more cheaply. Technology in this way revalues not only goods, but also all other factors out of which a goods are composed. Thus, for example, the Cotton Gin dramatically increased the volume and decreased the price of cotton, calling into action the hands, bodies of many times the slaves, and lands far more extensive than could be made efficient use of prior to its invention.

While neoclassical economic thinkers everywhere count the necessity of innovation of feature of capitalism, Marx counted it an abstract compulsion and immaterial form of domination. Obviously, African slaves did not “choose” to be transported across Louisiana into Texas; obviously, the Mexicans in Texas did not “choose” to “relocate”; obviously, the Native Americans did not “choose” to perish. But, nor did land developers and settlers “choose” to adopt the new technology, a technology that revalued their goods in such a manner that they had to expand their holdings or lose market share.

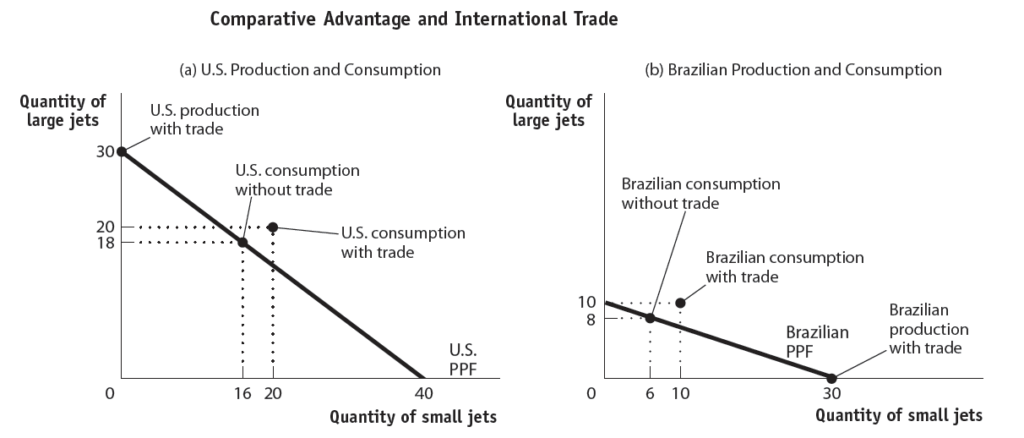

Because the underside of the production possibility frontier is the inefficiency and deadweight loss producers must bear if they do not fall into line with the dictates of the market. “Comparative advantage” means that a city, a region, and market can no longer afford to produce goods that it once produced and must, for the sake of economy, purchase goods produced elsewhere at a lower price. Only in terms of abstract value is this a win-win. But, let us say that diamonds or oil lie under the soil of my land. In that case, I not only enjoy a comparative advantage over other producers, but an “absolute advantage”:

To be sure, in the event that the costs of stealing a resource are higher than the benefit I anticipate deriving from it, there may nevertheless be a price I might pay to obtain rights to it. But the point, according to Marx, is that all goods and all actions are valued differentially within this closed universe in which all goods and all actions shape one another differentially.

Neoclassical economists capture this abstract form of domination and dependency in what is called the “Circular-Flow Diagram”:

In essence, the Circular Flow Diagram illustrates the comprehensive, rational, fully integrated character of the capitalist social formation. Any factor that can be capitalized — all factors have value — will be.

Perhaps most questionable in this chapter is Krugman and Wells distinction between “positive” and “normative” economics. Positive economics is descriptive. Normative economics lets policy makers know what they would need to do in order to achieve a specific policy outcome: healthcare, education, roads, investment, etc.

For the most part, Marx’s Capital is positive in the sense that Marx was eager to accurately characterize how capitalism works and to describe how it was working. Nevertheless, there was also a normative dimension of Marx’s economics, insofar as Marx theorized what kinds of policies would have to be implemented in order to practically isolate value from productive human action.

But — and this is absolutely critical — in his mature writings Marx denied either inevitability or necessity to this isolation of value from productive human action. In this sense, his critique was “negative” and neither “normative” nor “positive.” It indicated where neoclassical economists and policymakers failed to identify or factor in critical variables and sought to explain socially and psychologically why neoclassical economists might feel compelled to universalize or ontologize variables that, in his judgment, were better understood immanently, i.e., in their historical and social specificity, not as an eternal quality of human being (human ontology). Whether a community should choose, for example, to supply healthcare or housing or security or education to all of its members; yet, Marx was fully equipped to account for their reluctance to do so in terms of the abstract form of domination under which they made these “choices.”

That said, economists disagree. They use different models. They incorporate different variables into their models. They weight these variables differently. They ask different questions of the models they use. They make use of different data sets. While all of these choices and decisions are shaped by the abstract value form of the commodity, all economic thinkers, including Marxist economic thinkers, suffer from this disability. The best any of us can therefore do is select the best data and the best models to characterize existing economic action, to advise policy makers, or to show how existing or proposed policy is likely to shape economic action.

The problem with developing a Marxian Economics arises from the fact that Karl Marx did not intend to develop, nor did he develop, an approach to economics distinguishable from the neoclassical approach sweeping across Europe in the 1860s. What distinguished Marx’s approach to economics from, say, the approach of William Stanley Javons was that (1) Marx did not find it necessary to identify an independent variable, such as the public good, for example, to off-set the market; and (2) Marx held that since all values arose from socially and historically specific circumstances that were subject to change, recognizing and accounting for these changes could be, and needed to be made a part of economic thinking.

In place of an argument that this holds true, I take a standard neoclassical economic textbook — in this case Paul Krugman’s and Robin Wells’ Principles of Economics — and work through the text on Marxian grounds. My aim is not to cover all that Krugman and Wells write, nor all that Marx might have replied. My aim instead is to show that what distinguishes Marxian economic theory is not the principles of economics per se, but is the rigorous social and historical critique with which these principles needed to be supplemented.

The first chapter of Krugman and Wells’ Principles is divided into three subsections: (1) Individual Choice; (2) Interaction; (3) Economy-Wide Interactions. Krugman and Wells find that individuals need to make choices (a) because they cannot have everything; and (b) because resources are scarce. Because individuals do not have unlimited means to acquire everything they might want, they must weight their possible choices differentially. “The real cost of an item is its opportunity cost; what you must give up in order to get it.” This gives rise to the notion of a “trade-off,” when individuals compare a range of possible choices. Individuals will make the choice, say Krugman and Wells, that optimizes their marginal benefit. Individuals can be induced to make one choice over another through incentives.

Insofar as everyone does not have everything, individuals need to trade in order to obtain what they want in exchange for what they have. Because there are gains from trade, individuals will specialize in what they are willing to trade for what they want from others. In a close economy, where all individuals together produce what all individuals might want, an economy achieves equilibrium when everyone has made choices that reflect their opportunity costs and all individuals have concluded trades that maximize their marginal benefits; or, “when no individual would be better of taking a different action.” A market is judged “efficient” when it reduces the costs of reaching equilibrium to a minimum and when it maximizes the benefits of reaching equilibrium.

To these principles Krugman and Wells add two additional principles that appear to require independent variables: “equity” and “welfare.”

Equity is described as “fairness”; welfare invites us to consider “externalities,” costs external to the transactions between buyers and sellers.

We will return to these two independent variables.

When individuals exchange goods, they exchange the values of those goods to the parties of the exchange. Absent coercion, these values are necessarily equivalent. “One person’s spending is another person’s income.” This means that should the aggregate income of a market increases, but the volume of goods does not, this will increase the prices of the goods, but not the volume. If, by contrast, the aggregate income of a market decreases, but the volume of goods does not, this will decrease the prices of the goods, but not the volume. If income remains constant, but the volume of goods increases, this will decrease the prices of the goods; if the income remains constant, but the volume of goods decreases, this will increase the prices of the goods. Insofar as individuals invest in the production of goods at different moments, and insofar as incomes, the volume of goods, and prices only adjust to one another in the long run, it is virtually inevitable that individuals will invest in goods that later lose value, that individuals will accept a wage that loses value over time, and that more goods may be produced at a given cost than buyers at a later time are willing to shoulder.

Krugman and Wells therefore introduce a third independent variable: government intervention in markets: in the form of spending, taxes, and monetary supply.

How might Marx respond to Krugman and Wells’ text?

First, Marx would point out that choices are always socially and historically specific. Moreover, since the values of goods in any market are determined in aggregate, the trade-offs individuals must bear in mind are never and can never be static. Value often strikes individuals as a mechanism of their own personal, individual, desire. Yet, in economic terms, value is a market-wide social substance; a product of all of the decisions of individuals throughout the market. But this means, second, that marginal benefit is also never actually a private evaluation, since any individual’s maximization of their marginal benefit shapes the values of goods of individuals and the maximization of their marginal benefit. Equilibrium is then a supra-individual social form that holds for individual in particular, but everyone in general. It follows that an economy can be in equilibrium even when many individuals have not maximized their marginal benefit; or, put differently, even when what they take to be their marginal benefit has been determined by the choices of all other individuals within the market.

Marx would also point out that equity, in any rigorously mathematical sense, would apply only to the aggregate, not to individuals within the aggregate. Only if all individuals enjoyed the exact same resources, and only if these resources were regularly “reset,” could we say that equity applied individually. In reality, value in the abstract is always exactly equal to itself. Once it becomes a measure of goods, by definition these goods are differentially valued.

But, for this reason, Marx would also question the independent status of social or public welfare. If the private exchange does not actually generate the greatest good — efficient equilibria — then by what measure will this good be measured?

And, so the third independent variable: government. Is the government truly an independent variable? Imagine a government that owes no individual or party anything. Why would it act in one way and not another? Presumably it would in that case act according to some independent set of guidelines or rules. But why this set of guidelines or rules? Why not another? In the real world, governments are always composed by individuals who serve constituencies. Their service has a price. That price and its products are marginally related. Even where an agent or agency is “independent,” it is statutorily bound by rules and laws that are political.

But, finally, Marx would point out that marginalism only holds in societies where social relations are mediated by commodity production and exchange; where, that is, the values relating all things, all people, and all actions to one another are not independent. In societies where social relations are mediated by other kinds of values, things, people, and actions enjoy independence and therefore are either subject to custom and tradition or must be renegotiated again and again at each meeting.

So, for example, in the high Middle Ages in Europe, wages and prices were negotiated publicly among clergy, nobility, trades, and crown. Marginal values did not exist. In that case, the neoclassical economic model does not hold.

That said, and with these provisos, Marx would have little else to dispute with Krugman and Wells.