In chapter 4 of their Principles of Economics, Krugman and Wells take up Consumer and Producer Surplus.

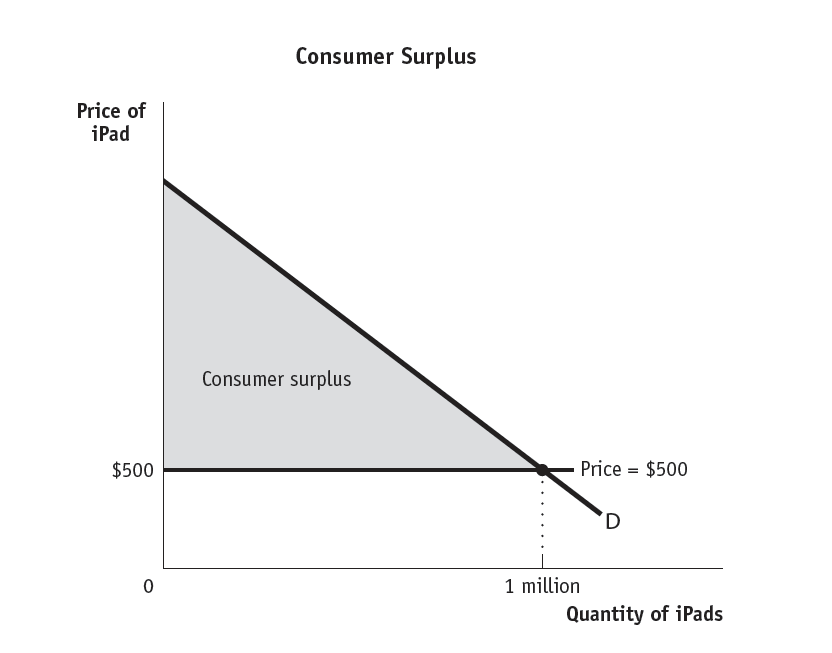

Consumers almost never pay the full price they would be willing to pay for a good. This follows from the fact that producers distribute goods and retailers price goods to attract not all potential consumers irrespective of their individual disposable income or desire for the good, but the optimum number of buyers at a specific price. Some buyers would be willing to pay substantially more. For some buyers, the retail price will be too great. The consumer surplus measures the value of a good for which consumers did not pay in aggregate.

It stands to reason that, as retailers price goods closer to their cost, this will increase the number of consumers eager to purchase those goods.

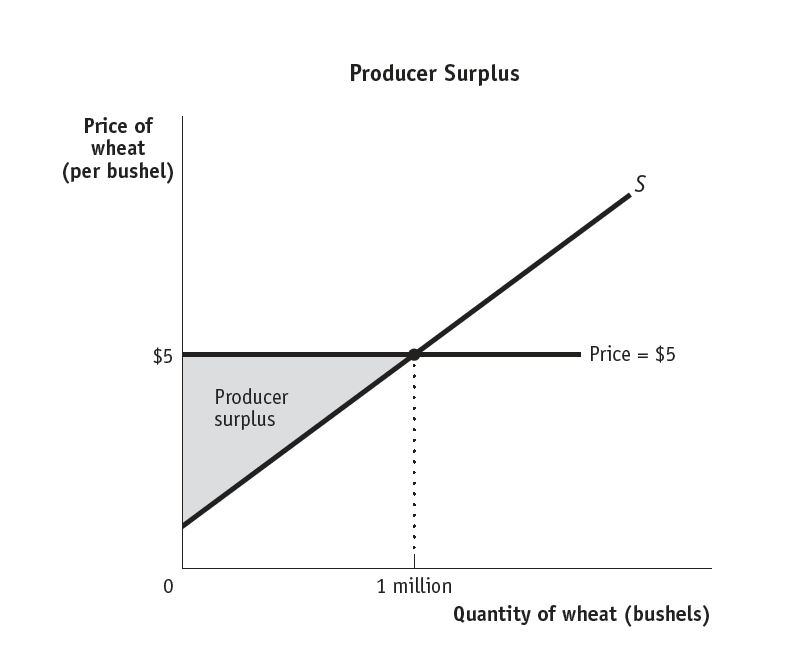

The same holds true for producers. Producers could sell a good at cost. As they increase the price they charge to retailers for a good, this will, by definition, decrease consumer demand. But producers rarely sell a good at cost. Producer surplus in aggregate equals the sum of the differences between cost and price.

It follows that as the price at which producers can sell a good increases, producers will produce more of that good. As the price declines, producers will produce fewer items.

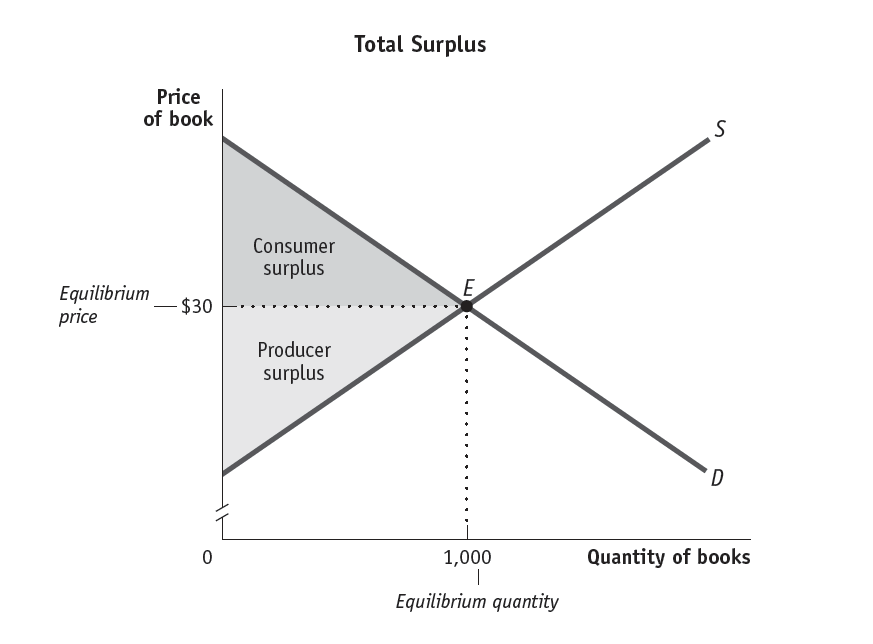

Total surplus falls where consumer surplus and producer surplus intersect:

But, again, we must emphasize that the triangles above and below equilibrium price are not evidence of exploitation. They are evidence rather of the abstract, immaterial character of value: value is not a quality in the substances out of which things are composed. Value is the abstract social substance that mediates social relations, i.e., in this instance, the social substance that induces publishers to print and distribute books and induces buyers to purchase them.

Equilibrium price is above the cost producers bear to produce books; equilibrium price is below the price consumers would pay for books. The area in both the triangles combined measures the total surplus or value won in aggregate by consumers and producers.

Krugman and Wells tell us that equilibrium price “allocates the good to potential buyers who value it the most” and “allocates sales to potential sellers who value the right to sell the good the most.” This requires some clarification. “Value” in this context needs to be understood as “value in the abstract.” Although, the meaning (sometimes deliberately, sometimes inadvertently) is ambiguous, value is, by definition, not a subjective quality of either buyer or seller. Thus, as Krugman and Wells note, an efficient market is not the same thing as a “fair” market; moreover, efficient markets do not please all consumers and producers all the time — by definition.

Krugman and Wells conclude the chapter by giving greater definition to market economies. Market economies are economies that grants an entity — public or private it makes no difference — the right to sell a good. So, for example, a public utility has the right to sell electricity (or water or gas, etc.). Producers and consumers rely upon signals — principally price — to help them make informed decisions.

Here Krugman and Wells discuss two concepts that require special attention: inefficient markets and market failure. Markets behave inefficiently when decisions to produce or consume are based on less than adequate signals to inform their decisions. So, for example, when central planners under “market socialism” decide how much bread to produce, the demand for bread at market price provides a less than adequate signal for determining how much bread to bake because the price is calibrated to the incomes of consumers and because the resources for baking bread are calibrated not to the cost of production but to the demand for bread. Value, under such circumstances, is subjected to substantive needs and conditions. Under normal circumstances, needs and conditions are subject to value.

Market failure is a much more problematic concept. So, for example, would we say that the market failed in 1929? Assets in 1928 adequately reflected what producers were willing to produce at prices consumers were willing to pay. Then in 1929 these assets lost considerable value because producers were unwilling to produce goods at prices consumers were willing to pay. The signals in both cases were clear. Consumers and producers relied in both cases on these signals. Insofar as this holds true, it is difficult to call 1929, the Crash, a market failure. The market “failed” only in one sense. The surface forms of appearance, the substances people wanted and needed, could not be procured at any price because the cost of producing these goods at any price exceeded the price consumers could pay. But, again, in what sense is this a “market failure”?

Krugman and Wells define market failure: “when a market fails to be efficient.” But is this really helpful? When producers stop producing a good — bread or PPE — because they cannot produce it efficiently, is this not instead evidence that markets work precisely as neoclassical economists predict they should?

Marx would fiercely dispute the notion that hunger, high unemployment, destitution, social unrest, or market turbulence provide evidence of market inefficiency or failure. Rather are they evidence that markets are performing precisely as they should perform.

But, what if public entities intervene to regulate production and consumption, let us say by heavily subsidizing the production of PPE or by providing universal, single-payer healthcare? There are two ways to think about public financing and regulation of production and consumption:

(1) by definition, they will place upward pressure on price. So, for example, when public entities elect to make war and provide funding to producers, public or private, to produce weapons and provide logistics, the RFP will infallibly place upward pressure on the price of the kinds of goods weapons and logistics producers provide and war-making publics consume. Regulation of prices and public oversight of production may help to keep prices lower than they would otherwise be. But, to the extent that war poses an existential threat, producers will likely push the marginal value of their goods in the direction of ∞, the value of all of the lives of citizens in a nation. But — and this is critical — public funding and regulation generate inefficiencies only because and insofar as they confirm the validity of the underlying market principles; and, so,

(2) we might also think about public funding and regulation along the lines (a) of any insurance scheme, whose costs decline in direct proportion to the range and volume of those covered; or (b) any public good, such as police or fire protection, whose value to all those covered declines as the proportion of covered to non-covered declines. In both of these cases, a greater efficiency is felt to arise from the inefficiencies accepted in a single sector or market. So, for example, free public education and training that extends from universities and trade schools to graduate studies spreads out the cost of a skilled and educated workforce throughout the entire population. It also dramatically increases the pool of highly skilled and educated workers from which employers, public and private, can choose, thus placing downward pressure on the wages any prospective employee can command or employer will offer; but since the work performed will be skilled, it raises the aggregate wages and benefits. The same obviously holds true for other public goods.

Neither of these instances requires that we adopt a different set of economic principles. Nor would Marx fault these principles for inadequately grasping how the capitalist social formation works. He would only object to Krugman and Wells’ definition of “market failure.”