In chapter six of their Principles, Krugman and Wells explain demand price and supply price elasticity. Intuitively, elasticity makes sense. A good that everyone needs (e.g., petrol, water, oxygen, health, food), regardless of price, will be demand price inelastic. A good that will be supplied in the same volume (e.g., nuclear warheads, grapes, PPE), regardless of price, is perfectly supply price inelastic. (How much are you going to pay for a nuclear warhead? If you want a nuclear warhead, you will pay . . . whatever.) In the long run, producers might shift cultivation from grapes to cannabis, but a change in price will not alter the volume of one or the other or both that a cultivator will supply. Only under highly unusual circumstances will a community elect not to supply its members with sufficient protective equipment to mitigate the spread of contagion, irrespective of price.

Again, what is perhaps most significant about elasticity is how accurately our neoclassical model captures actual market behavior. That is to say, what is remarkable is that human conduct lends itself to rigorous mathematical modeling. In particular:

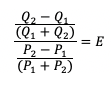

Where Q2 is the quantity of a good demanded following a change in price and Q1 is the initial price; and where P2 is the price corresponding to the quantity demanded following the price change and P1 is the initial price. In elasticity, again, consumers are not responding to the substances out of which things are composed. They are instead responding to a correlation between their need (however measured) and price — price, however, not as the cost of any thing out of which a good is composed, but as a multivariate calculation of their need measured against the needs and prices of all possible goods. Where E > 1 demand is elastic, i.e., it is responsive to price; where E < 1 demand is not elastic to price; and where E = 1, demand is unit elastic.

From which it follows that price elasticity is not only a factor of my “need,” but also the substitutes that might also satisfy this “need,” whether I judge the good a necessity or a luxury, but also, therefore, the elasticities of substitutes.

Consider the condition where a consumer is at risk purchasing food — often deemed a necessity — in her own neighborhood. Industry and high wage/high benefit employment left her neighborhood a long time ago, when the mines closed, when the factory moved off-shore, when manufacturing proved too expensive because healthcare costs are privately funded, when property prices declined, when policing turned against the residents, when the public elected not to fund schools, repair roads, maintain utilities . . . Consumers are at differential risks leaving their homes. They are also at risk entering other neighborhoods where the price of food might be less. For a variety of reasons, a consumer decides there is a higher marginal cost shopping outside her neighborhood. To this risk we might add opportunity cost. If we drives or takes mass transit to another neighborhood where prices are lower, the time and effort it takes her to travel, plus the risk, makes shopping locally relatively more attractive. But it also makes her behavior less price elastic. She will be willing to endure higher prices. Again, the question here is not whether “objectively” the higher prices she is ready to pay are offset by travel time and risk. The market, in aggregate, suggests that she will be ready to pay considerably higher prices for goods for which other consumers elsewhere pay less.

But, elasticity also tells us something about income. When a consumer is not constrained by income, price is less elastic; that is to say, consumers who enjoy more wealth than they need are less influenced by price changes than are consumers who must make decisions over whether to buy food or medicine, diapers or books, Internet or clothing.

For consumers who fall in the latter group, income elasticity shows up in the kinds of goods they purchase. Inferior goods are goods that sell in greater quantities when income drops. Normally, goods have a positive income elasticity. As income increases, consumers will purchase more of them. Inferior goods by contrast become more attractive when incomes fall.

Once again, Marx would entertain few objections to Krugman and Wells’ treatment. We can imagine conditions under which families do not have to choose between food or medicine. But we cannot imagine conditions in capitalist societies where price elasticity cannot be calculated or modeled and therefore where producers take consumer behavior as a signal for whether to produce more or less of some good. For example, we notice that when oil reserves plunge, prices climb. But, let us suppose that reserves climb. Since the price of petrol is relatively demand inelastic — i.e., since consumers will have to drive irrespective of the price — prices will never fall in line with supply.

For anyone therefore who thought that price or value were somehow hardwired into things, price elasticity or inelasticity should be enough to convince them otherwise.