In chapter 2 of their Principles of Economics, Krugman and Wells introduce trade-offs and trade. The chapter is divided into five sections: (1) introduces the concepts of modeling and caeteris paribus (all things being equal); (2) looks at the production possibility frontier, which identifies how producers decide what they should produce; (3) looks at comparative advantage or why all parties to trade can come out ahead; (4) looks at what is called the “circular-flow” diagram:

And lastly (5) which aims to distinguish between positive and normative economics. There is also a sixth section, which deserves separate treatment: when and why economists disagree.

As I mentioned in 1/32, so long as we remember that we should not be able to model human action using rigorous mathematical modeling, nothing would prevent or did prevent Marx from agreeing that human action in fully developed capitalist economies does lend itself to rigorous mathematical modeling. Caeteris paribus is also unnoteworthy. It simply shows that we are always selecting variables that we feel will most faithfully answer the question we are asking. We do not throw all existing variables at each question. Rather, we assume that all other things are equal.

To be sure, this can prove problematic, as when an economist assumes that wealthier individuals “prefer” better health, housing, and education than poorer individuals, since wealthier individuals “choose” better health, housing, and education than poorer individuals. Under such circumstances caeteris non paribus. Once we include systemic racism, institutional discrimination, and the “differential values” placed on different segments of the population, we will then discover that some of the variables left out of the model actually turn out to be critical. But the fault is not in caeteris paribus as a principle. The fault lies with researchers who exclude critical variables, or, more to the point, societies that value individuals differentially.

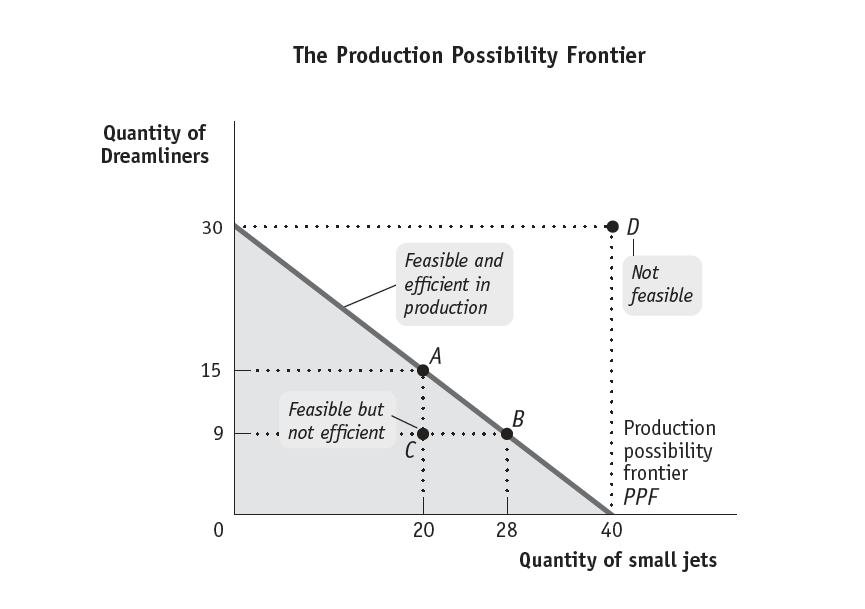

Nor would Marx, in principle, have problems with section two. In the simple model introduced by Krugman and Wells, we are invited to consider only two goods, Dreamliners (yes, no kidding) and small jets.

Since we cannot produce everything, there is some relationship between small and large jets. We could produce fewer of both (C), in which case we would lose six dreamliners we could have produced and eight small jets we could have produced. But we cannot under any circumstances produce 30 dreamliners and 40 small jets. Why? Because there are insufficient resources. Or, more specifically, because acquisition of sufficient resources would itself be inefficient. Why? Because available resources are measured in terms of the abstract value investors are willing to part with in order to develop a resource. Available resources are assumed constant in this model.

But let us suppose that investors invest in a technology whose cost proves lower than the value this technology earns by developing more resources? In effect, this new technology decreases the cost of developing a resource making it available more cheaply. Technology in this way revalues not only goods, but also all other factors out of which a goods are composed. Thus, for example, the Cotton Gin dramatically increased the volume and decreased the price of cotton, calling into action the hands, bodies of many times the slaves, and lands far more extensive than could be made efficient use of prior to its invention.

While neoclassical economic thinkers everywhere count the necessity of innovation of feature of capitalism, Marx counted it an abstract compulsion and immaterial form of domination. Obviously, African slaves did not “choose” to be transported across Louisiana into Texas; obviously, the Mexicans in Texas did not “choose” to “relocate”; obviously, the Native Americans did not “choose” to perish. But, nor did land developers and settlers “choose” to adopt the new technology, a technology that revalued their goods in such a manner that they had to expand their holdings or lose market share.

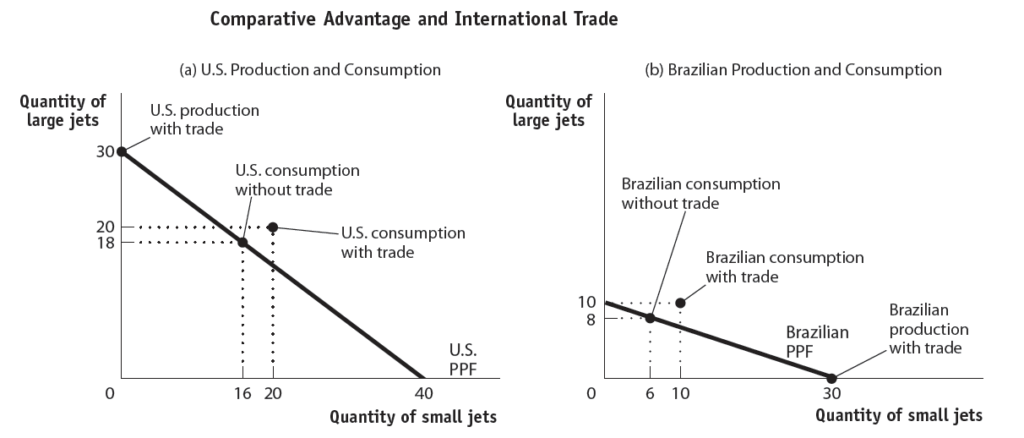

Because the underside of the production possibility frontier is the inefficiency and deadweight loss producers must bear if they do not fall into line with the dictates of the market. “Comparative advantage” means that a city, a region, and market can no longer afford to produce goods that it once produced and must, for the sake of economy, purchase goods produced elsewhere at a lower price. Only in terms of abstract value is this a win-win. But, let us say that diamonds or oil lie under the soil of my land. In that case, I not only enjoy a comparative advantage over other producers, but an “absolute advantage”:

To be sure, in the event that the costs of stealing a resource are higher than the benefit I anticipate deriving from it, there may nevertheless be a price I might pay to obtain rights to it. But the point, according to Marx, is that all goods and all actions are valued differentially within this closed universe in which all goods and all actions shape one another differentially.

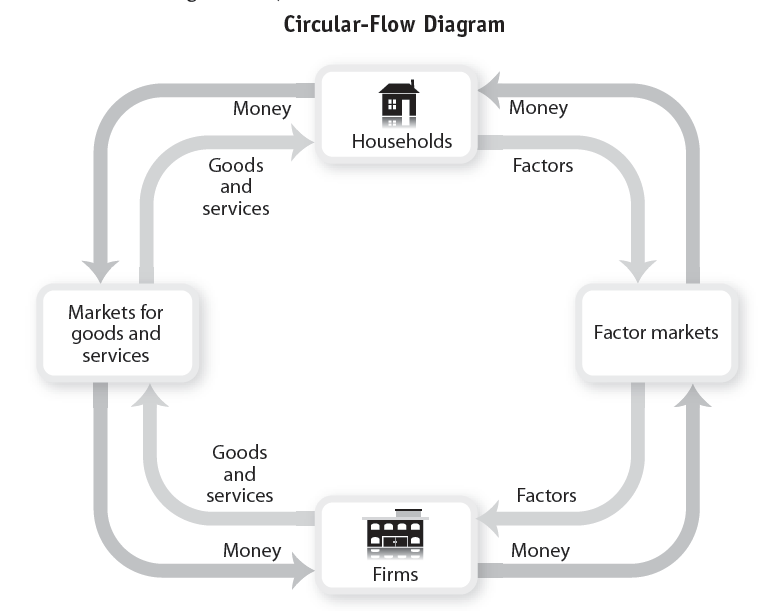

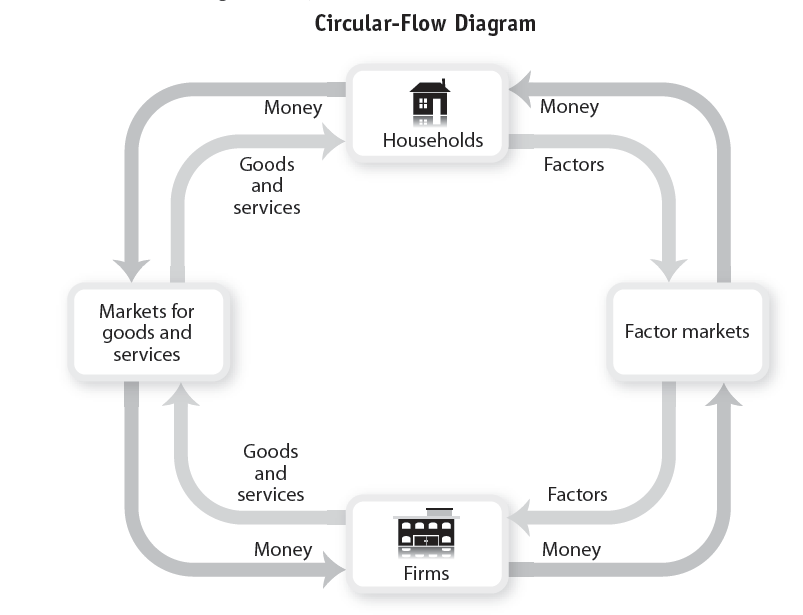

Neoclassical economists capture this abstract form of domination and dependency in what is called the “Circular-Flow Diagram”:

In essence, the Circular Flow Diagram illustrates the comprehensive, rational, fully integrated character of the capitalist social formation. Any factor that can be capitalized — all factors have value — will be.

Perhaps most questionable in this chapter is Krugman and Wells distinction between “positive” and “normative” economics. Positive economics is descriptive. Normative economics lets policy makers know what they would need to do in order to achieve a specific policy outcome: healthcare, education, roads, investment, etc.

For the most part, Marx’s Capital is positive in the sense that Marx was eager to accurately characterize how capitalism works and to describe how it was working. Nevertheless, there was also a normative dimension of Marx’s economics, insofar as Marx theorized what kinds of policies would have to be implemented in order to practically isolate value from productive human action.

But — and this is absolutely critical — in his mature writings Marx denied either inevitability or necessity to this isolation of value from productive human action. In this sense, his critique was “negative” and neither “normative” nor “positive.” It indicated where neoclassical economists and policymakers failed to identify or factor in critical variables and sought to explain socially and psychologically why neoclassical economists might feel compelled to universalize or ontologize variables that, in his judgment, were better understood immanently, i.e., in their historical and social specificity, not as an eternal quality of human being (human ontology). Whether a community should choose, for example, to supply healthcare or housing or security or education to all of its members; yet, Marx was fully equipped to account for their reluctance to do so in terms of the abstract form of domination under which they made these “choices.”

That said, economists disagree. They use different models. They incorporate different variables into their models. They weight these variables differently. They ask different questions of the models they use. They make use of different data sets. While all of these choices and decisions are shaped by the abstract value form of the commodity, all economic thinkers, including Marxist economic thinkers, suffer from this disability. The best any of us can therefore do is select the best data and the best models to characterize existing economic action, to advise policy makers, or to show how existing or proposed policy is likely to shape economic action.