In chapter five of their Principles of Economics, a chapter subtitled “meddling with markets,” Krugman and Wells look at price controls and quotas. To repeat, my aim in this series is not to disclose an occult Marxian way to pursue economics, but rather to show how Marx was in nearly all respects a fairly straightforward neoclassical economic thinker. The matter of price controls and quotas is a case in point. Insofar as commodity production and exchange aim to produce and expand value, any intervention into production or exchange that impairs or impedes this production or expansion in order to achieve some end other than production and expansion is, by definition, an impediment to market efficiency.

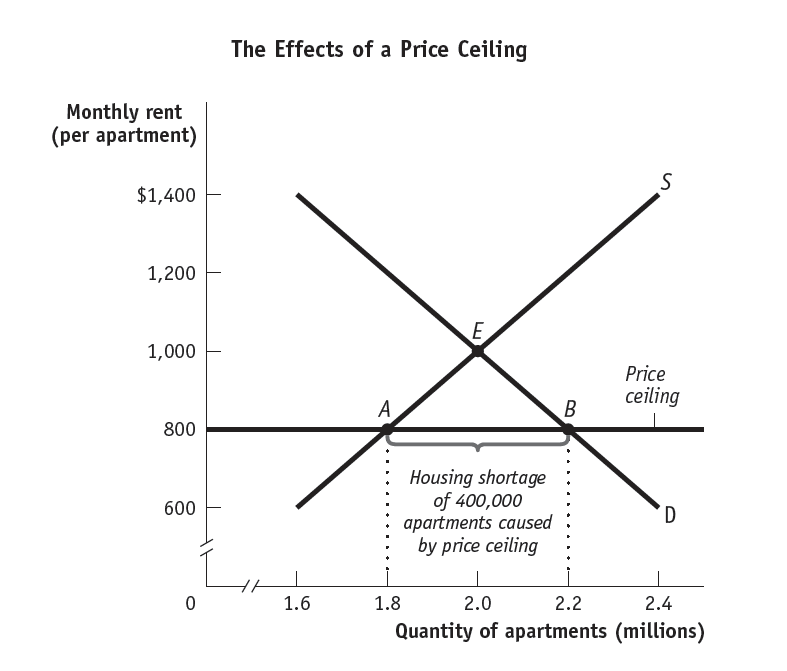

So, for example, some entity might wish to make rents more affordable and to this end might place a ceiling on what property owners can charge renters to let rooms, apartments, or homes.

In this example, where property owners could charge $1000 per unit, they would place 2M units on the market, where supply and demand intersect (E). Should an entity limit to $800 per unit the price property owners could charge, demand for $800 units would increase to 2.2M, but property owners would, at that price, only be willing to place 1.8M units on the market, giving rise to 200K fewer units than would have been let at market price (E) and 400K fewer units than were demanded at the rent-controlled price.

Economists call the shortfall “deadweight loss.” They call the lag in supply an “inefficient allocation to consumers.” Moreover, since producers will take units off the market that might otherwise be available, and since consumers will be compelled to seek alternative housing, resources will be wasted. Also, the units that property owners will be willing to place on the market will hold values no greater than $800. You get what you pay for.

But let us say that your professor has an in-law unit she is willing to rent to you for $1200 “off the books.” Price ceilings also therefore give rise to so-called “black markets.”

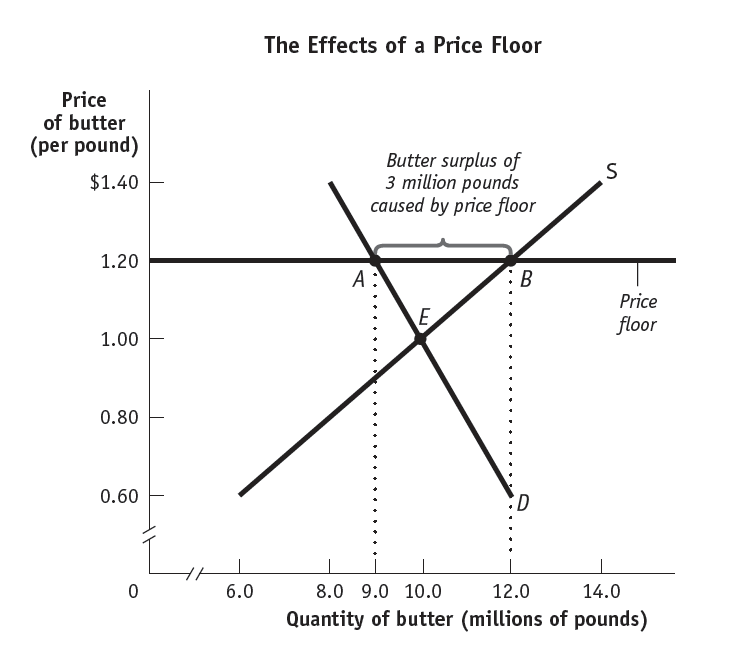

Price floors have a similar effect on markets. Let us say, for example, that more consumers would purchase a good were its price permitted to fall to equilibrium, but that fewer producers would be willing to produce a good at its equilibrium price:

At equilibrium, therefore, producers produce only 10M lbs of butter when butter is only $1/lb. Yet, should some entity fix a lower boundary on what producers can charge, in this case $1.20/lb, producers will be willing to produce more butter, 2M lbs more butter, but consumers will demand 1M lbs less butter than they would at equilibrium, and will demand 3M lbs less butter at $1.20 than producers are willing to supply at that price.

Once again, the effect will be deadweight loss, since the quantity bought and sold will be lower than it otherwise would be; an inefficient allocation of sales, since producers will be deterred from entering a market where demand has declined; and unnecessarily high quality will prevail, since consumers would otherwise be willing to pay less for a lower quality of good. And, just as in price ceilings, so price floors give rise to illegal activity.

Where price floors and ceilings make use of the price mechanism, quotas make use of quantities. Krugman and Wells illustrate the effect quotas have on markets by showing what happens when a city limits the number of taxis that can operate on its streets. (New Yorkers must bear quietly with this example.)

At equilibrium 10M riders would be willing to hail cabs for fares of $5/ride. By limiting the number of cabs available for hire to 8M, the regulatory authority has selected a point on the supply curve that suggests a fare of $4/ride. But, in fact, with the dearth of cabs, riders are now willing to pay $6/ride, a dollar more than equilibrium, which is good for all of those able to afford a medallion. The “wedge” indicates the “rent” riders pay for the limit placed on number of cab drivers. But, let us say that I find a cab driver operating outside of the law. And let us say that she will charge me $5/ride until she learns that I am with the regulatory agency, at which point she drops the fare even further. Or take another example.

Land owners in the Central Valley of California are always eager to drive down wages for seasonal agricultural workers. One way to drive down wages would be to open the border between Mexico and the US to workers who, generally, are willing to accept a lower wage than domestic laborers. (This, for example, is how Germany has solved its shortage of healthcare and waste management workers.) But, since legal workers in the US enjoy greater protections than workers in Mexico, Central Valley land owners would have to compensate migrant seasonal laborers from Mexico at a much higher wage than they are willing to pay. Placing a strict quota on documented workers would appear then to deprive Mexican migrant laborers who are willing to work access to employment and deprive Central Valley land owners laborers to work their farms. But, let us now say that regulators turn a blind eye to land owners who hire undocumented workers; and let us say that land owners deprive undocumented workers legal protections in exchange for allowing them to work. In this case, quotas that are selectively enforced can create what has been called the $1.25 apple. Normally, were workers paid a living wage, that same apple would cost $25 — providing an incentive for growers to mechanize their industry. As it is, absent a wage floor, consumers get the best of both worlds: an affordable apple.

Here again, Marx would find little to dispute in Krugman and Wells’ analysis. Insofar as social relations in capitalist societies are mediated by the production and exchange of commodities, goods are produced not in order to satisfy desire for goods, but in order to satisfy desire for abstract value. Where the marginal product has been limited by any external constraint — a price floor, price ceiling, or quota — producers and consumers are compelled to compensate for their loss by making other choices. So, for example, in the case where immigration from Mexico is legally constrained, growers wishing neither to mechanize their production nor charge $25 per apple are instead forced to find ways around the law. Your professor is forced to rent out her in-law unit beyond the reach of regulatory authorities. And medallion owners trade in medallions priced at several years’ income.

Where Marx would object is in the conceit that markets are ever unconstrained. In order to function at all, markets always operate under constraints. As the above examples illustrate, value is no law-abiding citizen. It is always in search of the shortest distance between two points, the law notwithstanding. The question, therefore, is (1) how will policy makers and enforcers select the constraints that constrain markets; and (2) who will bear the cost of the inefficiencies generated by these constraints?

Consider the case of rent control. By holding rents down, there is greater demand than private owners are willing to supply. But let us then suppose that the producer of some good — a university for example — nevertheless gains value from a steady and growing supply of tuition-paying-units. Or, more generously, let us say that a state — California for example — finds value in a highly educated and innovative workforce. In that case, either of these entities should be willing up to the margin, to make up for the deadweight loss arising from rent control. Or, in the alternative, California could highly subsidize public higher education in general, allowing institutions such as UC Berkeley, to offer a four-year education for free, making more disposable income available for other uses, such as rent. Or, both of these entities could coordinate their efforts in any number of ways. But why?

In Marx’s view, the only reason any of these entities would take any of these steps would be to increase the value of their marginal product. In no case would they elect to do so should it flatten or depress their marginal product. Public health and education increase aggregate marginal value. Yes. Of course. Which means that they pose no threat to the capitalist social formation.